")

Yum China: Insider buying and valuation ratios make the stock a strong buy (NYSE:YUMC)

Subscribe

Yum China Holdings, Inc. (NYSE: YUMC) offers an attractive buying opportunity following strong second-quarter 2024 results and a significant accumulation of insider buying activity in the days following the results release.

In this article I will guide you through the I will discuss the various aspects of my investment thesis and try to convey as directly as possible the various events that led to my Strong Buy recommendation.

Additionally, I’ll go through some of the headwinds heading into Q2 2024, particularly their strategic move with Pizza Hut WOW, which I believe poses a risk to my Strong Buy rating in the event of an economic downturn.

However, since my time frame is relatively short (three to 24 months), I am convinced that this stock offers asymmetric opportunities in the short to medium term.

As always, I start with a section about the company for those readers who are not yet familiar with this stock.

Company overview

Yum China is a Shanghai-based company that operates a large number of restaurants in China and focuses on fast food and casual dining.

They have exclusive rights to operate and sublicense the KFC, Pizza Hut and Taco Bell brands in China.

In addition, they own the intellectual property rights to two brands, Little Sheep and Huang Ji Huang. These two names may not be familiar to you unless you have been to China recently.

They generate most of their revenue from their KFC and Pizza Hut restaurants. To give you an idea of the relative weight of each segment, I have included a breakdown of their annual revenue in 2023 below.

| segment | Sales 2023 (in millions) |

|---|---|

| KFC | $8,240 |

| Pizza Hut | $2,246 |

| All other segments | $779 |

| Corporate and unassigned | $293 |

Author’s compilation from the most recent 10-K issues.

As a side note, all other segments include sales from brands such as Lavazza, Huang Ji Huang, Little Sheep and Taco Bell, their delivery business segment and their e-commerce business.

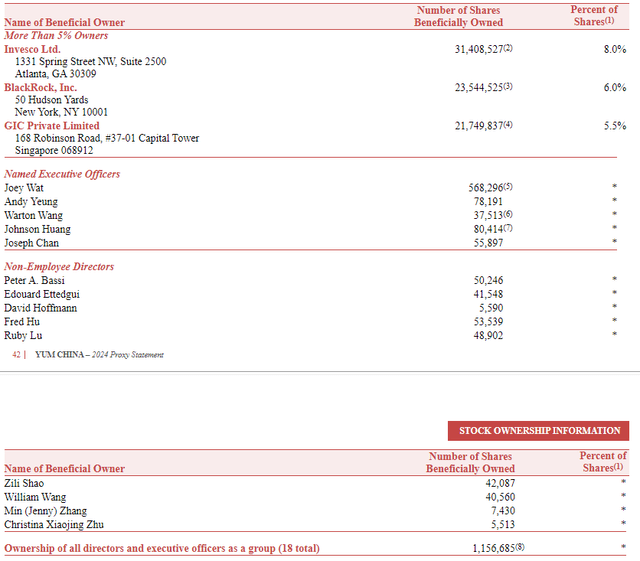

With regard to the beneficial owner (As of April 11, 2024) of the Company, I must admit that I am disappointed by the fact that the total ownership of all directors and officers of the Company is less than 1%.

§ 14A SEC-14F

However, my investment style is based more on insider buying (especially after a recent sell-off) than on owning all of the company’s common stock.

If you’re wondering why that is, it’s because my time frame is relatively short, between three and 24 months, and mostly with very illiquid call options. So when I see a cluster of insider buying after a stock price decline, I firmly believe that management thinks the current stock price is cheap. (Emphasis on current)However, if insiders own 40% of the company but don’t buy after a sell-off, I can’t make the same argument.

Current performance

I like to start my dinner with cake, so I’ll address the headwinds first, despite the decent second-quarter 2024 results.

My investment style favors companies with high margins and low revenues, especially while maintaining flexibility during economic downturns. Since it is taken for granted that fast food restaurants are more concerned with revenues than increasing their margins, I thought I would take a closer look at their strategic initiatives. One of them, the Pizza Hut WOW concept, caught my eye.

This concept was developed to appeal to a wider audience, especially those who eat alone and are price-conscious. The basic idea is that by offering smaller portions and cheaper meals, Pizza Hut WOW meets the needs of a wider audience who prefer to eat alone or are looking for a quick meal at a reasonable price.

I’ll be honest, there’s nothing wrong with that. I was born in a socialist country, so I like it from an ethical point of view. More people eat more, at cheaper prices, which means more workers are needed to meet the increased demand.

However, from a purely economic perspective, I do not believe this will have a positive impact on their net income in the long term, especially in the event of an economic downturn.

Considering that operating expenses for the Pizza Hut segment were $460 million, I see the 13.2% margin at risk in the event of a downturn in the QSR industry.

Just to be clear, I’m not saying there will be a downturn in the QSR sector, but if that happens, I think Pizza Hut’s margins will be at risk.

Now, moving on to more positive results, I must mention that in terms of revenue, it was a record-breaking second quarter. Their total revenue was $2.68 billion, up 1% year over year.

Operating profit increased 4% year-on-year, and total operating margin was 9.9%, also an increase from the prior-year quarter, albeit only by 20 basis points.

I’m also encouraged by their 11% year-over-year increase in delivery sales. Incidentally, nearly 90% of their total sales came from digital sales, via digital fast food ordering apps.

outlook

Let’s take a quick look at the stock price in the weekly chart.

Trading View

As a contrarian deep value investor, I like this chart for the following reasons:

- Year-to-date decline (prior to Q2 2023 results) of 33%.

- Looking further back, the share price has fallen by over 50% since April 2023.

- The price recovered from what I believe to be a validated support level from 2019.

Okay, the chart looks good, but that’s just the tip of the iceberg.

Let’s get to the finances.

Operating profit has increased, which is good.

Trading View

I am also encouraged by the increased operating and net profit margins since 2022.

Trading View

Liquidity and liquidity ratios above 1 and a debt-to-asset ratio below 0.5, which I believe is a good indicator that they can manage both their short-term and long-term debt.

It pays a quarterly dividend, with a low dividend yield of under 2% TTM. This is a good sign as they do not have to give up a significant portion of their free cash flow to pay dividends.

Speaking of cash flow: both operating cash flow and free cash flow have increased.

Trading View

In terms of valuation, I like the fact that most valuation metrics are below the company’s five-year average. Since the company operates in the Chinese market, I don’t place much emphasis on comparisons with the broader consumer goods sector.

So the weekly chart shows a sell-off, financial reports look decent, and valuation ratios are below the five-year average (great!). Now I’m going to focus on insider buying activity.

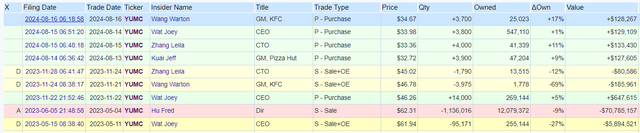

I thought about attaching a screenshot showing the cluster’s significant insider buying activity after the 20% increase in share price following the second quarter results (emphasis on after).

OpenInsider

The results were released on August 5 after the market closed. Insiders began buying between August 13 and 16.

I find it very encouraging that the five purchase transactions were carried out by five different insiders, including the CEO, CFO and GM of their two largest segments.

This is the perfect scenario for my investment style. All the factors I look for are positive, so I decided to take a bold step and buy call options expiring in January 2025.

If my strong buy recommendation does not hold true, my portfolio will take a hit.

Diploma

In summary, I believe Yum China represents an attractive buying opportunity, especially for risk-taking, contrarian investors like me.

Although Pizza Hut’s margins are at high risk in the event of an economic downturn, the company’s overall financial health is robust, with increasing revenues and operating margins and strong cash flows.

Compared to their own five-year average, their valuation ratios seem pretty decent to me, suggesting they may be undervalued.

Insider buying activity, particularly by top executives, and the 33% decline in the share price since the beginning of the year further reinforce my confidence in the current share price.

Therefore, I maintain my “Strong Buy” rating and hold call options expiring in January 2025.

is a “strong stock”")

")