stock recover after earnings release?")

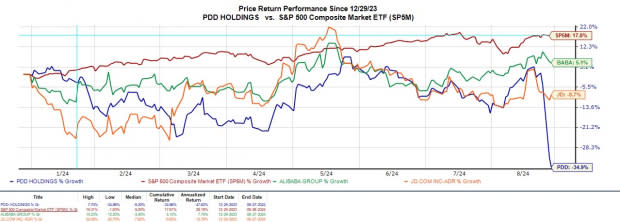

PDD Holdings PDD has been one of the better performing stocks in recent years, but has fallen 30% since announcing second-quarter results on Monday. The sharp sell-off comes after the multinational e-commerce company reiterated that a decline in its profitability is inevitable and expects that trend to begin in the third quarter.

Tougher competition and greater economic concerns are expected in China, although PDD’s discounts can help it take market share from other e-commerce giants such as Alibaba BABA. and JD.com JD.

Image source: Zacks Investment Research

PDD’s second quarter results

PDD reported second-quarter revenue of $13.35 billion, which missed estimates by 2%, although it was up 85% from $7.2 billion in the comparable quarter. On the bottom line, second-quarter earnings per share of $3.20 were 10% better than expected and up 122% from $1.44 per share a year ago.

Notably, PDD has beaten the Zacks EPS Consensus for 14 consecutive quarters and posted an average earnings surprise of 41.14% in its last four quarterly reports.

Image source: Zacks Investment Research

PDD’s growth curve

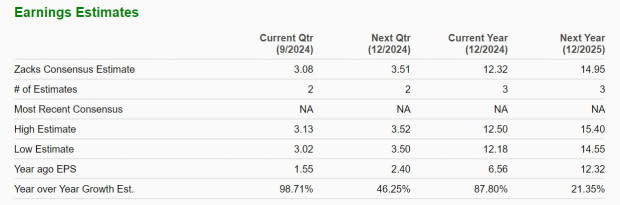

According to Zacks Estimates, PDD’s total revenue is expected to increase 62% to $56.27 billion in fiscal 2024 from $34.64 billion in the previous year. PDD’s revenue is expected to increase another 27% to $71.59 billion in fiscal 2025.

Annual earnings are expected to rise 87% to $12.32 per share this year, compared to earnings per share of $6.56 in 2023. Additionally, earnings per share are expected to rise another 21% in fiscal 2025. However, it is notable that earnings estimate revisions for fiscal 2024 and 2025 may start to decline following PDD’s reiteration of its warning of lower profitability.

Image source: Zacks Investment Research

Rating comparison

At $95, PDD stock trades at an earnings multiple of 8.1, a significant discount to the 23.7x multiple of the S&P 500. Moreover, after the recent decline, PDD now trades near 9.4x to Alibaba but above 6.5x to JD.com.

Image source: Zacks Investment Research

Conclusion

Following its second-quarter report, PDD Holdings stock earns a Zacks Rank #3 (Hold). While it may be tempting to buy PDD stock after the earnings beat, the company is beginning to suffer the same fate as many other Chinese e-commerce companies that appear to be undervalued but have sunk into volatility due to general economic fears.

Given its expansive growth curve, PDD is certainly a profitable long-term investment, but even better buying opportunities may arise in the future.

Want the latest recommendations from Zacks Investment Research? Download the 7 best stocks for the next 30 days today. Click here to get this free report

PDD Holdings Inc. Sponsored ADR (PDD): Free Stock Analysis Report

JD.com, Inc. (JD): Free Stock Analysis Report

Alibaba Group Holding Limited (BABA): Free Stock Analysis Report

To read this article on Zacks.com, click here.

Zacks Investment Research