A reader asks for a continuation to an earlier blog post:

Do you have an inverse chart showing what bonds do when the market goes up (which happens much more often than when it goes down)?

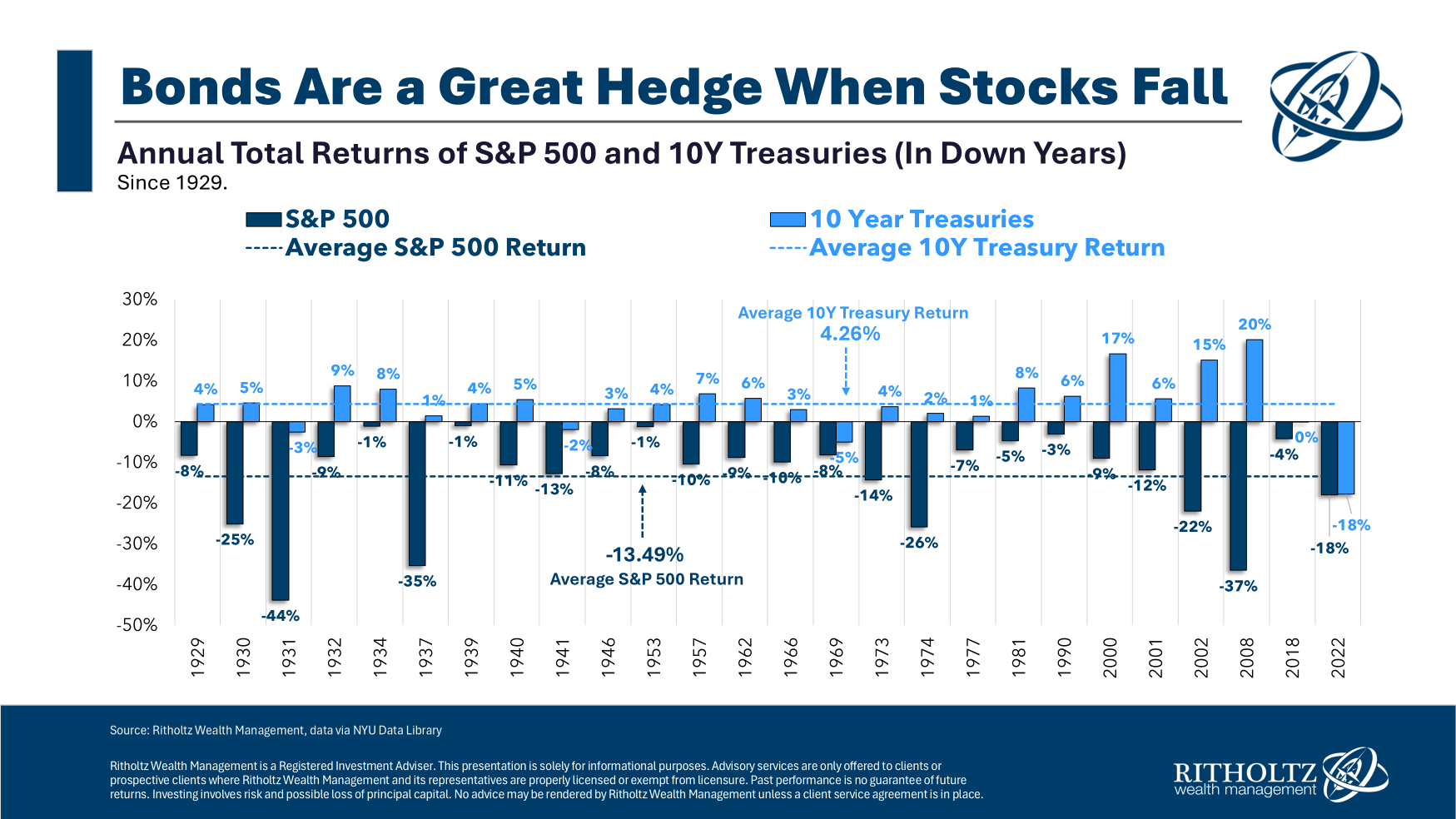

Recently I looked at the historical performance of bonds when stock prices were falling:

In summary, bonds usually rise when stock prices fall – but not always.

High-quality bonds are a pretty good hedge against bad stock market years.

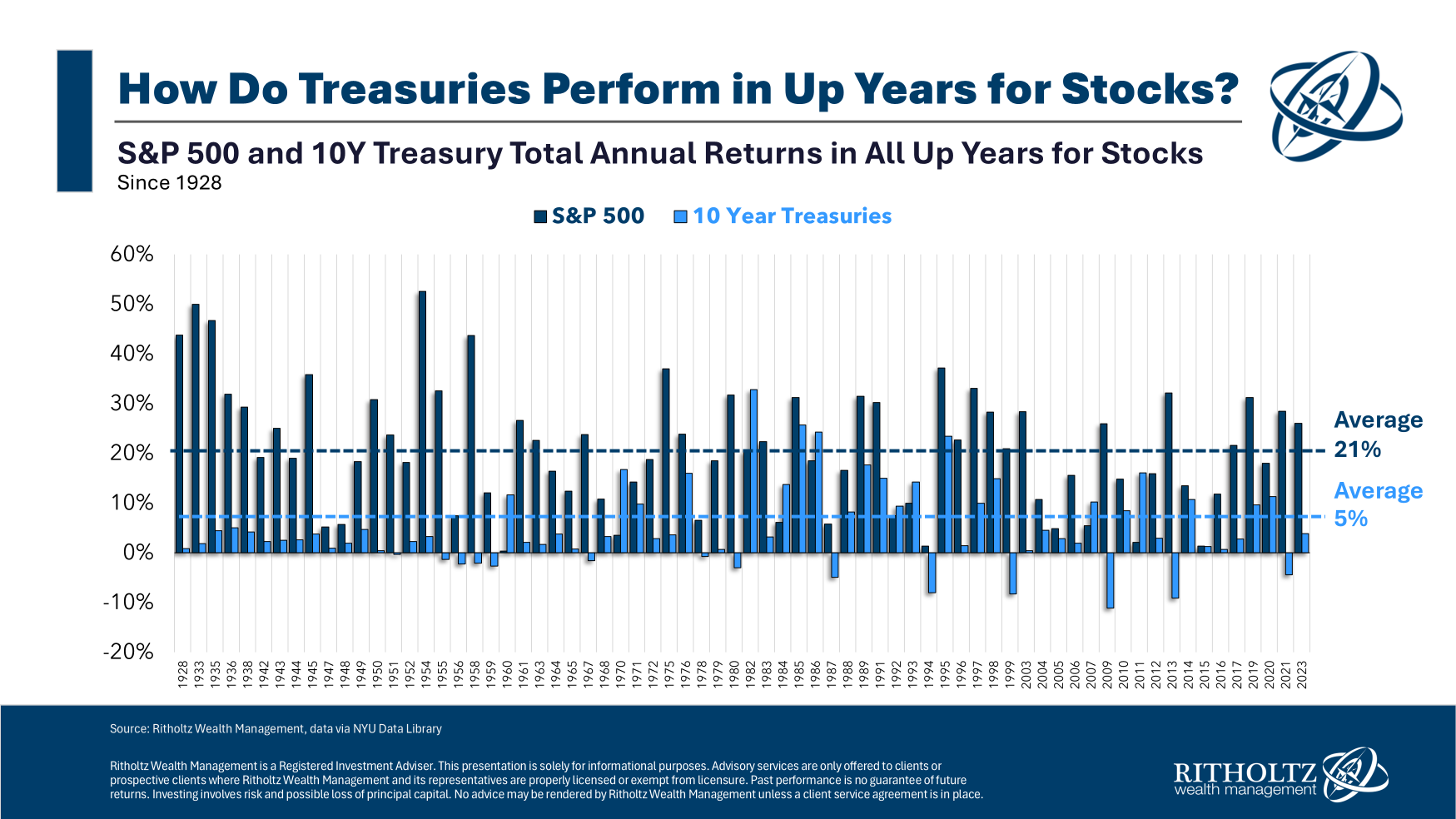

I’ve never looked at the other side of this question: How do bonds perform when the stock market rises?

Here’s a look at every positive year for the S&P 500 along with the corresponding 10-year Treasury yield since 1928:

Some investors mistakenly assume that there is a negative correlation between stocks and bonds, meaning that when stocks rise, bonds fall and when stocks fall, bonds rise.

But bonds have performed well during the stock market’s up years.

In fact, average yields on 10-year government bonds were higher in good years than in bad years:

Bonds are obviously far more stable than the stock market. The distribution of bond gains and losses has been similar during stock market upswings and downswings.

When the S&P 500 was positive, bonds had negative returns 20% of the time (which means 80% positive results).

When the S&P 500 was down, bonds had negative returns 19% of the time (which translates to 81% positive returns).

Average returns were similar and win/loss ratios were similar.

What does this tell us?

Bonds are quite good for diversification.

Of course, there are market environments where bond and equity correlations can hurt a portfolio. The most recent example was 2022, when both stocks and bonds fell in a rising interest rate/inflation environment.

Diversification works most of the time, but not always.

It is also interesting to look at the average gains and losses on the stock and bond markets.

The average up year for the stock market was a gain of over 20%, while the average down year saw a loss of over 13%. For bonds, the average up year was +7.1%, while the average down year saw a loss of -4.9%.

Bonds have also been positive overall for more years than stocks.

From 1928 to 2023, 10-year Treasury bonds ended the year with a gain 80% of the time, while the stock market rose 73% of all years during that period.

These numbers provide a good explanation for the risk premium inherent in the stock market. The stock market delivered more than double the annual return of bonds over the 96-year period from 1928 to 2023, in part because owning stocks entails higher risk.1

On the stock market, profits are higher, but so are losses.

You cannot earn a risk premium without taking some risk.

The good news for diversified investors is that there can be a time and a place for both asset classes.

In nearly 60% of cases, stocks and bonds ended the year with gains at the same time. In 36% of all years, bonds ended the year higher than stocks.

In the long run, the stock market wins, but in the short term, this is not always the case.

Bonds are in positive territory most of the time, regardless of whether stock prices are rising or falling.

Not perfect, but fixed income remains one of the easiest ways to hedge the stock market.

We addressed this question in the latest edition of Ask the Compound:

My colleague Alex Palumbo joined us on the show this week to discuss questions about how to deploy a large portion of cash savings, how to diversify company stocks, how to evaluate financial performance and how to think about alpha when choosing a financial advisor.

Further reading:

The Holy Grail of Portfolio Management

1The S&P 500 rose 9.8% annually, while 10-year Treasury bonds rose 4.6% annually between 1928 and 2023.

This content, which contains security-related opinions and/or information, is for informational purposes only and should not be considered as professional advice or an endorsement of any practice, product or service. No warranty or representation can be given that the views expressed herein are applicable to any particular facts or circumstances and should not be relied upon in any way. You should consult your own advisors regarding legal, business, tax and other related matters relating to investments.

The comments in this “post” (including all associated blogs, podcasts, videos and social media) reflect the personal opinions, views and analysis of the Ritholtz Wealth Management employees making those comments and should not be considered as the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of the advisory services provided by Ritholtz Wealth Management or the performance returns of any Ritholtz Wealth Management Investments client.

References to securities or digital assets or performance data are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. The charts and graphs contained therein are for informational purposes only and should not be relied upon when making investment decisions. Past performance is not an indicator of future results. The content is only as of the date indicated. Any projections, estimates, forecasts, objectives, prospects and/or opinions expressed in these materials are subject to change without notice and may differ from or contradict opinions expressed by others.

Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payments from various companies for advertising in affiliated podcasts, blogs and emails. The inclusion of such advertising does not constitute or imply an endorsement, sponsorship, recommendation of the same, or any association therewith by the content creator or Ritholtz Wealth Management or any of its employees. Investing in securities involves risk of loss. Additional advertising disclaimers can be found here: https://www.ritholtzwealth.com/advertising-disclaimers

Please view the disclosures here.

stock? – Applied Mat (NASDAQ:AMAT)")