")

Anastasia Yakovleva

Note:

Valaris Limited (NYSE:VAL) previously, so investors should view this as an update to my previous articles on the company.

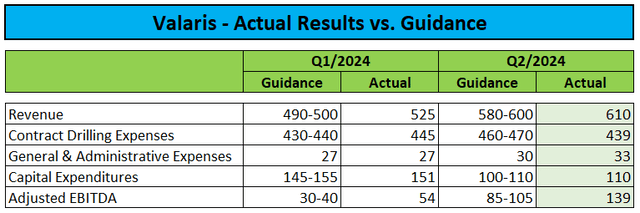

Two weeks ago, leading offshore driller Valaris reported strong second-quarter results. Sales and profit results significantly exceeded management forecasts:

Transcripts of conference calls

The outperformance is due to very high revenue efficiency combined with a number of contracts that ran longer than expected. In addition, the results benefited from the postponement of certain costs to subsequent quarters.

Company press releases/official documents

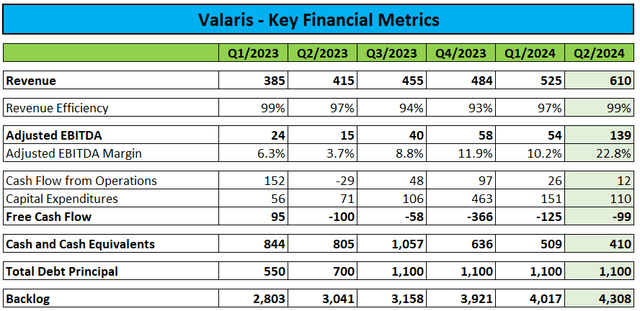

Revenue of $610 million and adjusted EBITDA of $139 million reached new multi-year highs. The adjusted EBITDA margin of 22.8% more than doubled from the previous quarter.

However, free cash flow remained negative due to a combination of higher working capital requirements and increased capital expenditure, albeit at 410 Liquidity remains strong with $1.5 million in cash and cash equivalents and an undrawn credit facility of $375 million.

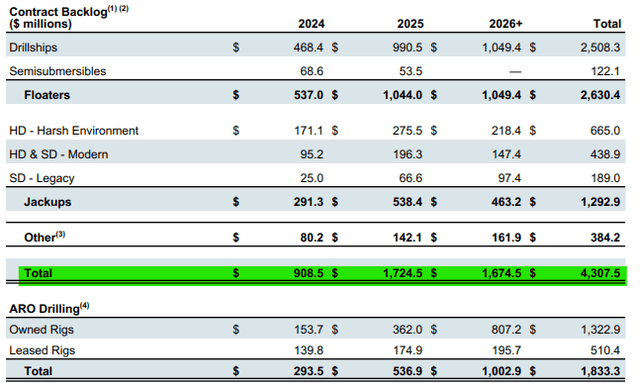

The backlog increased 7% quarter-on-quarter to $4.3 billion, primarily due to the recently announced award of a multi-year contract for the drillship. Valaris DS-17 Offshore Brazil:

Fleet status report

Please note that the backlog does not include ARO Drilling, the Company’s unconsolidated joint venture with Saudi Aramco (ARMCO).

Unfortunately, Saudi Aramco recently decided to suspend the jack-up contracts Valaris 147 And Valaris 148as stated by management in the conference call:

Discussions are currently ongoing with Aramco where there are other rigs leased by Valaris where our owned rigs could be affected by the suspensions instead of Valaris 147 and 148, and the effective date of these suspensions. While we currently expect the suspensions could negatively impact our full-year 2024 EBITDA by up to $10 million, these two contracts represent only $35 million of our $4.3 billion backlog.

Taking a step back, Saudi Aramco’s suspension of construction of up to five additional rigs does not change our market assessment, as they represent approximately 1% of the global jack-up rig fleet on the market.

While the financial impact will be limited, the suspensions will result in further short-term idle time for the Company’s fleet after the semi-submersible drilling rig Valaris DPS-5 and the drilling ship Valaris DS-10 have concluded their respective contracts in recent weeks, with limited short-term opportunities for follow-up work despite Valaris DS-10 It is a high specification 7th generation drillship.

In addition, the jack-up platform Valaris 249 will be out of service for several weeks due to necessary repairs:

Regarding the Valaris 249, the rig recently sustained leg damage while being driven off site prior to its next assignment. We currently estimate that the rig will be out of service for several weeks to make the necessary repairs and that the total financial impact including downtime and repair costs will be between $5 million and $10 million.

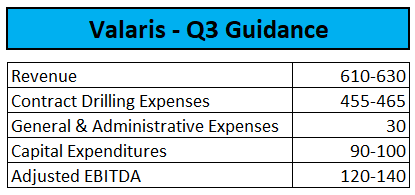

Although there will be some offsetting factors, profitability is expected to decline quarter-on-quarter despite an expected increase in revenue:

Transcript of the second quarter conference call

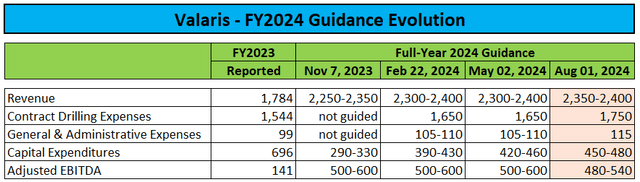

Worse still, management significantly lowered its profitability forecast for the full year:

Transcript of the second quarter conference call

In the conference call, management attributed the weaker outlook to the lack of follow-on orders for Valaris DPS-5 And Valaris DS-10necessary repairs to Valaris249 and the recent contract suspensions for Valaris 147 And Valaris 148.

However, the Company expects cash flow to improve in the second half of the year due to a combination of higher day rates and lower expenses for reactivations and contract preparations.

Management also reaffirmed its commitment to return capital to shareholders:

Looking ahead, we expect to generate significant and sustainable free cash flow in 2025 and beyond and intend to distribute all future free cash flow to shareholders unless there is a better or more value-enhancing use for it.

While the Company remains optimistic about the long-term prospects of the industry, the slowdown in contracting activity observed at Valaris in recent quarters is expected to result in increased idle time on a number of rigs, which in turn will impact profitability and cash flow.

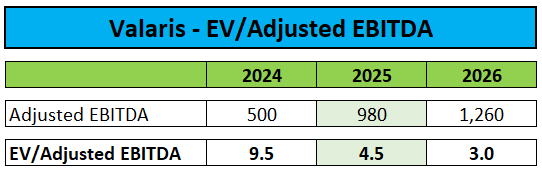

Since we do not expect contract activity to pick up until the second half of next year, I have lowered my adjusted EBITDA estimates by 10% for 2024 and by about 7% for 2025:

Author’s estimates

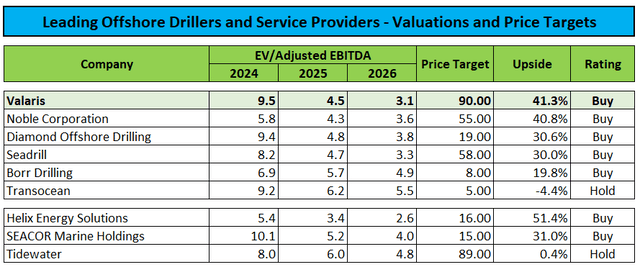

However, since the company’s asset value is already significantly devalued compared to its US-listed peers, I have only slightly reduced my price target from $92 to $90.

DNB Markets

Given an upside potential of more than 40% from my revised price target, I confirm my “Buy” Valuation of shares.

Author’s estimates

Conclusion:

While Valaris reported acceptable second-quarter results, the recent slowdown in contract awards combined with further contract suspensions by Saudi Aramco and damage to a jack-up rig prompted management to cut its full-year profitability expectations by about 10%.

Since a revival in contract activity is not expected before the second half of next year, I have reduced my estimates and my price target accordingly.

However, even taking into account the subdued short-term outlook, Valaris is still expected to see a significant increase in its profitability and cash generation next year.

Given the company’s commitment to returning capital to shareholders, I would expect Valaris to resume share buybacks and possibly introduce a quarterly dividend in the not too distant future.

Given an upside potential of more than 40% from my revised price target of USD 90, I reiterate my “Buy” Valuation of shares.