It is NVIDIA‘S (NASDAQ: NVDA) World, investors just live in it. At least that’s how it felt in 2023 and 2024. The chipmaker and leading provider of artificial intelligence (AI) computing infrastructure now has a market cap of over $3 trillion, making it the third-largest company in the world. With a gain of nearly 3,000% over the past five years, it’s now one of the best-performing stocks of all time, making long-time shareholders incredibly wealthy.

I expect this monster run to be over soon. No, it has nothing to do with the company’s upcoming earnings release on August 28. But it does have to do with a growing competitive environment that could affect Nvidia’s pricing power in the long term. For this reason, I believe Nvidia’s monster stock gains will end in the next few years.

Vertical cloud integration

Nvidia’s operating profit has grown more than 2,000% to $48 billion over the past five years. This growth is due to Nvidia chips being the primary computing instrument for new AI tools sweeping the technology sector. As the only scaled supplier of these best-in-class chips and with a technological edge over competitors such as IntelNvidia has seen an increase in revenue and profit margins as the company sells these scarce resources at astronomical prices.

Three of his biggest customers are Amazon, alphabet (Google) and Microsoft. These are the three major cloud computing providers that form the infrastructure backbone for new AI algorithms and software. Together, these three probably spend over $10 billion a year, maybe even $20 billion, on Nvidia chips. Now it looks like Nvidia has upset the cloud hornet’s nest.

In a move that’s received little attention on Wall Street, these cloud providers have announced huge investments in making their own AI chips. For example, Amazon now makes its own chips called Inferentia and Trainium, which compete directly with Nvidia. The products currently lag behind Nvidia’s in terms of processing power, but with so much money being spent on Nvidia chips, it makes sense for Amazon to pour billions of dollars into research and development to try to improve those offerings.

Google has its own tensor processing units (TPUs) and Microsoft has announced investments in internal chip development. It may take years for these to scale, but supply will only increase and mean more competition for Nvidia, not less. Worse still, the competition comes from Nvidia’s own customers.

Competition eliminates pricing power

A key to Nvidia’s stock gains over the past two years has been the increase in operating margin. From a low of just under 15%, Nvidia’s operating margin has risen to around 60% over the past 12 months. This has actually contributed more to Nvidia’s profit growth than revenue. Revenue has grown 228% over the past three years, while operating margin has increased almost fourfold from its low.

Nvidia can enjoy absurd profit margins because it currently has little competition in AI computer chips. This creates pricing power that accelerates revenue growth and expands margins – a wonderful combination of catalysts for a stock. But this can be reversed if competition increases, which is what is happening with the three largest cloud providers. If they continue to replace more and more of their Nvidia chips with their own brands, Nvidia’s revenue and profit growth will be hurt.

To be clear, the timeline for this competition is not 2024. It may take several years for Amazon, Microsoft and Google to put a dent in Nvidia’s AI chip business. But the companies have a huge incentive to do so because Nvidia has imposed price increases on them. All three major cloud providers have plenty of money to spend to get these businesses to size. And they’re working on it.

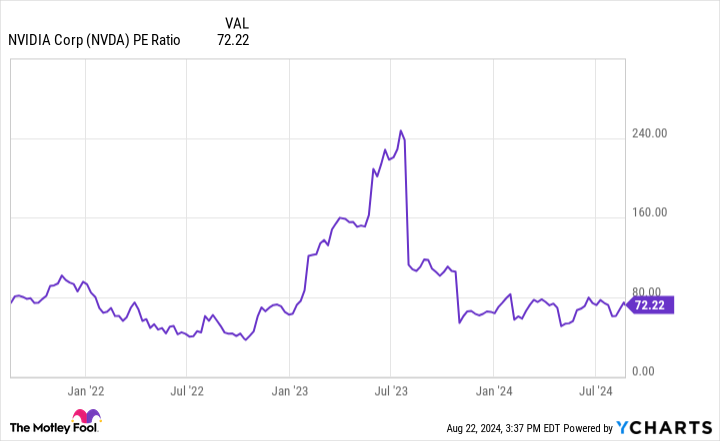

NVDA P/E data from YCharts.

Risks for Nvidia shares

Nvidia stock has incredible momentum right now. That’s because earnings and revenue are growing at an incredible rate. A growing supply of AI chips from competitors – be it Amazon or anyone else – could be a double headwind for Nvidia’s finances.

Growing competition means that the supply of chips that cloud providers and other AI chip buyers can buy is increasing. The simple law of supply and demand states that if supply increases but demand stays the same, prices will fall. This would lead to a decline in revenue and a reduction in margins, both of which would negatively impact Nvidia’s profitability.

Today, Nvidia is trading at a price-earnings ratio (P/E) of 73, which is almost three times the S&P500 Index average. And this is based on trailing earnings with sky-high profit margins of 60%. If pricing power weakens, it will impact revenue And Profit margins. In numerical terms, this means that profits could be significantly lower even if Nvidia sells more computer chips in the coming years.

Stocks with declining earnings don’t trade at a P/E of 73. And remember, that P/E would jump to over 100 compared to the current $3 trillion market cap if profit margins fell to “only” 40%. That makes Nvidia stock incredibly risky, which is why I predict its huge stock run is coming to an end. It’s still a quality company, but not one that deserves to trade at a $3 trillion market cap right now.

Should you invest $1,000 in Nvidia now?

Before you buy Nvidia stock, consider the following:

The Motley Fool Stock Advisor The analyst team has just published what they believe to be The 10 best stocks for investors to buy now… and Nvidia wasn’t among them. The 10 stocks that made the cut could deliver huge returns in the years to come.

Consider when NVIDIA created this list on April 15, 2005… if you had invested $1,000 at the time of our recommendation, You would have $792,725!*

Stock Advisor offers investors an easy-to-understand plan for success, including instructions on how to build a portfolio, regular updates from analysts, and two new stock recommendations per month. The Stock Advisor Service has more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of August 22, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, a subsidiary of Amazon, is a member of The Motley Fool’s board of directors. Brett Schafer has positions in Alphabet and Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Prediction: This will put an end to Nvidia’s huge stock gains was originally published by The Motley Fool