Most investors are interested in Energy transfer (NYSE:ET) are attracted by the high yield, which currently stands at 7.9%. The company currently pays a quarterly distribution of $0.32 and aims to increase this by 3-5% annually in the future.

That’s attractive in and of itself, but I also think the pipeline operator’s share price could almost double in the next five years.

This could happen through a combination of growth projects and a moderate increase in the share price if investors assign a higher valuation to a stock.

Let’s see why I believe Energy Transfer’s share price can more than double in the next five years.

Growth opportunities

Energy Transfer is one of the largest midstream companies in the United States and has an extensive integrated system that spans the entire country. The company operates in virtually every area of the midstream sector, transporting, storing and processing various hydrocarbons through its systems. The size and breadth of its systems provide it with numerous opportunities for expansion projects.

This year, the company plans to invest between $3 billion and $3.2 billion in growth capital expenditures (capex) on new projects. Going forward, it could spend between $2.5 billion and $3.5 billion per year on growth capital expenditures to pay the distribution while also having money left over from cash flow to pay down debt and/or buy back shares.

With this in mind, and given the early opportunities Energy Transfer sees in power generation due to the increasing power demand of data centers as a result of the advent of artificial intelligence (AI), it is probably safe to assume that the company could spend approximately $3 billion annually on growth investments over the next five years.

Most midstream companies target a minimum 8x multiple for new projects. This means that the projects would pay for themselves in about eight years. For example, a $100 million project with an 8x multiple would generate an average return of $12.5 million in EBITDA (earnings before interest, taxes, depreciation and amortization) per year.

Based on this type of return from growth projects, Energy Transfer should be able to increase its adjusted EBITDA from $15.5 billion in 2024 to approximately $17.4 billion in 2029 if the company continues to spend $3 billion annually on growth projects.

Numerous expansion options

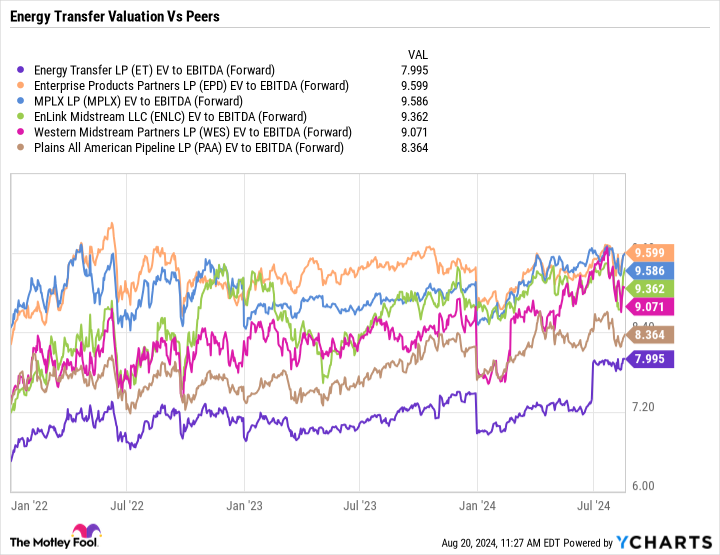

From a valuation perspective, Energy Transfer is the cheapest stock among its midstream peers in the master limited partnership (MLP) segment. It trades at 8x forward enterprise value to adjusted EBITDA. This metric takes into account a company’s net debt minus non-liquid items and is the most commonly used method for valuing midstream companies. At the same time, the company trades at a much lower value than it has in the past.

MLP Midstream stocks averaged an EV/EBITDA multiple of 13.7 between 2011 and 2016, so the multiple for the industry as a whole has declined. However, with demand for natural gas increasing due to AI and falling demand for electric vehicles, the transition to renewable energy could potentially take much longer than expected. If that’s the case, these stocks should be able to command a higher multiple than they currently do, as it reduces fears that demand for hydrocarbons will decline significantly in the coming years.

How Energy Transfer’s share price almost doubled

If Energy Transfer grows its EBITDA as expected, the stock could reach $30 in 2029 if the company can achieve an EV/EBITDA multiple of 10x. While that’s more than the 8x forward and 8.7x trailing multiple it currently commands, it’s still well below what the MLP midstream space has historically achieved.

|

2024 |

2025 |

2026 |

2027 |

2028 |

2029 |

|

|---|---|---|---|---|---|---|

|

Adjusted EBITDA |

15.5 billion US dollars |

15.88 billion US dollars |

16.25 billion US dollars |

16.63 billion US dollars |

17.0 billion US dollars |

17.38 billion US dollars |

|

Price at 8x multiplier |

$17 |

$18 |

$19 |

$20 |

$21 |

|

|

Price at 9x multiplier |

21,50 € |

22,50 € |

23,50 € |

24,50 € |

$25.50 |

|

|

Price at 10x |

$26 |

$27 |

$28 |

$29 |

$30 |

* Enterprise value is based on 3.42 billion shares outstanding, $57.6 billion in debt, $3.9 billion in preferred stock, $3.9 billion in investments in unconsolidated subsidiaries and cash, and $11.6 billion in minority interests.

However, Energy Transfer and several other midstream companies appear very well positioned to become stealth AI winners due to increasing demand for natural gas power. Energy companies and data centers have already approached Energy Transfer about natural gas transportation projects, and there could be a natural gas volume boom. Given these growth opportunities, along with the company’s strengthened balance sheet and steady sales growth, I could see Energy Transfer’s multiple increasing slightly over the next five years and its stock price nearly doubling.

But even if the price-to-earnings ratio doesn’t increase, investors can still earn a very solid return through a combination of distributions (currently $0.32 per share per quarter) and more modest price appreciation. Without a price-to-earnings ratio increase and distributions above $7 between now and the end of 2029 (assuming 4% annual appreciation), the stock would still return over 75% over that time period.

Should you invest $1,000 in Energy Transfer now?

Before you buy Energy Transfer shares, consider the following:

The Motley Fool Stock Advisor The analyst team has just published what they believe to be The 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could deliver huge returns in the years to come.

Consider when NVIDIA created this list on April 15, 2005… if you had invested $1,000 at the time of our recommendation, You would have $792,725!*

Stock Advisor offers investors an easy-to-understand plan for success, including instructions on how to build a portfolio, regular updates from analysts, and two new stock recommendations per month. The Stock Advisor Service has more than quadrupled the return of the S&P 500 since 2002*.

View the 10 stocks »

*Stock Advisor returns as of August 22, 2024

Geoffrey Seiler has positions at Energy Transfer, Enterprise Products Partners, and Western Midstream Partners. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.

Forecast: Power transmission equipment inventory will nearly double in 5 years was originally published by The Motley Fool