Meta Platforms (META) is arguably the best stock in the Magnificent Seven right now and offers a buying opportunity in my opinion. The social media company’s advertising revenue and user base continue to grow and its valuation leaves plenty of room for error. Its recent earnings report and long-term performance make me optimistic about the stock.

Net income increases without job cuts

Meta Platforms’ net income has risen sharply in recent quarters, prompting the social media giant to declare its first quarterly dividend this year. Earnings continued to trend in that direction, posting a 73% year-over-year increase in the second quarter.

Efficiency has been a key factor in the company’s rising profits. That’s code word for laying off more employees, but there were no significant cuts this quarter. While the first quarter of 2024 saw a 10% year-over-year decline in headcount, the second quarter saw only a 1% year-over-year decline in that area.

Meta Platforms’ ability to retain employees while maintaining robust net income growth may position the company well for the future. One downside to laying off large numbers of employees is the loss of talent and the difficulty of replacing those who leave. That this downside was less pronounced in the second quarter while net income continued to grow is an encouraging development.

Daily active users continue to increase

Facebook, Instagram and WhatsApp are three of the major social media platforms – all owned by Meta. Although these platforms are well known, they continue to attract new users. Meta Platforms reported a 7% year-over-year increase in daily active users across its family of apps. Due to high user growth, the company closed the quarter with 3.27 billion daily active users.

A growing user base allows meta platforms to provide more ad placements for businesses, small businesses and influencers. These additional ad placements can help meta platforms achieve increased revenue growth for several years.

A good rating

The valuation of a stock is an important part of the analysis after looking at the fundamentals. Meta Platforms definitely delivers with a P/E ratio of 27.5. There are many companies with a similar valuation that do not offer their investors 73% annual net income growth.

Alphabet (GOOG) (GOOGL) is the only stock in the Magnificent Seven trading at a lower valuation, and its annual net income growth pales in comparison to Meta Platforms. In addition, Facebook’s parent company should continue to benefit from rising revenues and profits, which should drive its P/E ratio even lower.

It’s also good to know that Meta Platforms’ net income growth has outpaced its share price gains year-to-date. Meta Platforms stock is up 49% year-to-date, helped by rising earnings.

A dividend growth story in the works

Meta Platforms is not just aimed at growth investors. The company’s recent dividend program now makes it an attractive choice for dividend growth investors. Although Meta Platforms only yields 0.37%, it has the financial growth and liquidity to support an annual double-digit dividend growth rate for many years to come.

Meta Platforms ended the quarter with $58.08 billion in cash. The company has enough resources to support dividend increases over time, but Meta Platforms does not even need to dip into those reserves for the dividend program.

The company paid out $1.27 billion in dividends to its investors this quarter. In the same quarter, Meta Platforms allocated $6.32 billion for share buybacks. Shifting some of the buyback funds into dividend payouts is enough to increase the dividend by at least 10% per year for several years, but for tax purposes, it is better for the capital to go toward share buybacks.

While we’ve been looking at Meta Platforms’ net income growth rate, the company’s total GAAP earnings for the quarter were $13.5 billion. That’s enough money to support increased dividends for years to come. So Meta Platforms has the makings of a dividend growth stock that will outperform the market while growing its dividend significantly over the years. This setup should attract many dividend investors as it becomes more apparent.

Is META stock a buy according to analysts?

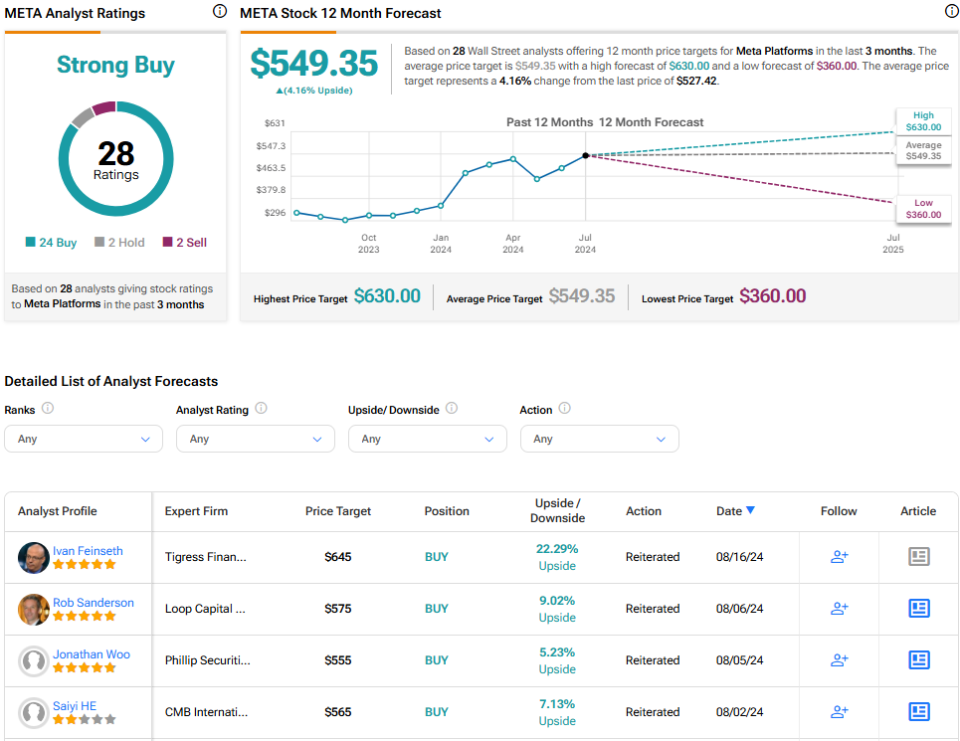

Meta Platforms is currently rated as a strong buy on TipRanks based on 24 buy recommendations, two hold recommendations and two sell recommendations over the past three months. The average price target for META shares suggests 4.2% upside from current levels, but that reflects Meta Platforms’ recent gains. The highest price target of $645 per share assigned today suggests the stock can gain another 22% from current levels.

View more META analyst ratings

The conclusion on meta-platform stocks

Meta Platforms has provided its investors with incredible revenue and net income growth over the past few quarters. Additionally, rising profit margins have lowered the stock’s P/E ratio, although it has continued to outperform the market. Additionally, Meta Platforms continues to grow its user base, which will lead to higher revenue in the future.

It was encouraging to see Meta Platforms grow its net income 73% year over year while retaining most of its employees. This is a sign that the company is not relying on job cuts to generate more profit. Many analysts believe that Meta Platforms can continue to generate profits for long-term investors, and I agree with them.

notice

:max_bytes(150000):strip_icc()/MarketBlogImage-final-6ac06c7b9250446a8e86c566b11e02e1.png "Major indices slightly down as stocks look to continue their winning streak")

– Stay Invested")