")

Full Truck Alliance: Positive due to strong second quarter growth and favorable volume forecast (NYSE:YMM)

Justin Paget

Full Truck Alliance Co. Ltd.‘S (NYSE: YMM) Shares are still rated Buy based on my assessment of the company’s performance and prospects. YMM achieved revenue and earnings growth rates of over +30% year-on-year in the last quarterThe company expects its order volume to increase by at least +20% for the full 2024 financial year.

In my previous update on May 24, 2024, I evaluated YMM’s shareholder return and key financial metrics for the first quarter of 2024. In the current report, I look at Full Truck Alliance’s second quarter results and full year outlook.

Financial performance in Q2 2024 was good

YMM’s revenue and normalized net profit attributable to shareholders increased strongly by +34% YoY and +33% YoY to RMB2,764 million and RMB954 million, respectively, in the second quarter of this year. These figures were released in Full Truck Alliance’s latest quarterly earnings release.The company’s actual revenue and normalized earnings in the second quarter of 2024 beat their respective consensus estimates by +2% and +1%, respectively, according to data from S&P Capital IQ.

In my previous article on May 24, 2024, I pointed out that YMM “with the measures it has taken to increase transaction service revenue, such as introducing the ‘commission model’ in more Chinese cities and leveraging ‘big data analytics,’ is likely to continue to show good results in the second quarter.” I was right, as Full Truck Alliance’s transaction service revenue increased 63% year-on-year to RMB 952 million in the second quarter of 2024.

In its corporate presentation slides, YMM explains that its revenue stream from transaction services refers to the “monetization of truckers related to our freight brokerage service” in the form of a “commission charged per transaction.” The proportion of Full Truck Alliance orders that were charged commissions increased from 67% in Q2 2023 to 81% last quarter, the company announced on its Q2 2024 earnings call. This suggests that the company has been successful in expanding the geographic coverage of the “commission model” mentioned above, which has resulted in a significant increase in transaction services revenue.

The company’s operating margin improved by +340 basis points year-on-year from 21.9% in Q2 2023 to 25.3% in Q2 2024. In releasing its second quarter results, YMM attributed the improvement in profitability in the last quarter to “revenue optimization and operating leverage.”

The revenue contribution (as a percentage of total revenue) for Full Truck Alliance’s transaction services revenue stream increased from 28% in the second quarter of last year to 34% in the second quarter of this year. I previously mentioned in my May 24, 2024 report that “YMM’s transaction services revenue stream has relatively higher margins than its other revenue streams.” Therefore, a positive change in Full Truck Alliance’s revenue mix has increased its profit margins in the second quarter of 2024.

On the other hand, YMM’s revenue growth accelerated from +24% in Q2 2023 and +33% in Q1 2024 to +34% in Q2 2024. Faster revenue growth on a fixed cost basis resulted in positive operating leverage effects, which had a positive impact on the company’s profitability in the second quarter.

In summary, Full Truck Alliance achieved good results in the second quarter of the current year.

Continued strong order volume growth is expected for the full year 2024

Full Truck Alliance’s order fulfillment increased by +22% year-on-year to 49.1 million in the second quarter of 2024, and YMM forecast a full-year order fulfillment increase of at least +20% in its second quarter earnings call.

A “growing trucking user base” was cited as the primary driver for YMM’s second-quarter order volume increase, according to the company’s Q2 2024 earnings call commentary. Specifically, Full Truck Alliance’s monthly active trucking users, or MAUs, increased +33% year-over-year to 2.7 million last quarter.

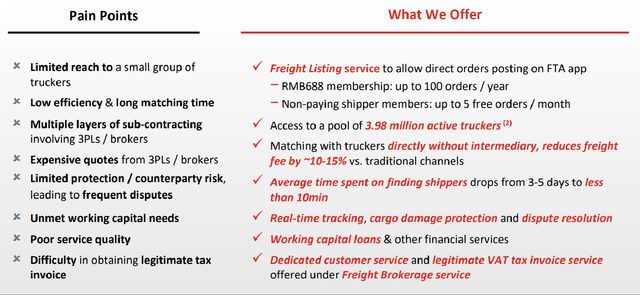

How YMM alleviates the “pain points” for shippers

Full Truck Alliance Corporate Presentation Slides

It is expected that Full Truck Alliance will be able to continue to increase the number of carriers on its digital freight platform. As highlighted in the graphic above, YMM’s digital freight platform offers several solutions to address the challenges faced by carriers. It is also worth highlighting that the number of new carriers who completed their first transaction on YMM’s platform reached a new historical high in the second quarter of 2024. (Source: Earnings Discussion.)

According to consensus data from S&P Capital IQ, sell-side analysts currently expect YMM’s revenue to grow +25% to RMB 10,538 million in fiscal 2024. This is consistent with the company’s actual fiscal 2023 revenue growth of +25%.

In short, Full Truck Alliance is well positioned to maintain strong revenue growth in the current year, comparable to the actual revenue increase achieved in the previous year. This is realistic considering the growing number of shippers at YMM, which supports the forecast for order volume growth of +20% or more for the full year.

Variant view

A slower than expected increase in the percentage of Full Truck Alliance orders on which commissions are charged could negatively impact YMM’s transaction services revenue growth and revenue mix going forward.

Weaker than expected order volume growth resulting from a more moderate increase in the number of shippers could have an adverse impact on the Full Truck Alliance’s future order volume.

These are the two main risk factors that will impact my bullish thesis for the stock.

Diploma

Full Truck Alliance currently trades at 13x trailing twelve-month normalized P/E based on valuation data from S&P Capital IQ. In contrast, YMM’s non-GAAP net income attributable to shareholders grew +33% year-over-year, and the sell-side expects the company’s normalized net income to grow +25% per year over the 2023-2027 period.

YMM’s strong second-quarter results and positive outlook suggest the stock could potentially trade at a more demanding P/E of 20 or better. This would be closer to actual earnings growth in the second quarter (+33%) and the expected earnings growth rate for the next four years (+25%). Therefore, I maintain a Buy rating on Full Truck Alliance.