")

FS KKR: Strong price fluctuations as long as high yields are still on offer (NYSE:FSK)

Paper Boat Creative/DigitalVision via Getty Images

FS KKR Capital (NYSE: FSK) Investors have endured significant market volatility over the past two weeks as the stock fell to lows last seen in early May 2024. I expect the market frustrated by the expected decline in interest rateswhich could affect the future development of net investment income per share. In addition, significant sell-off on the markets The decline in the FSK triggered by the settlement of the yen carry trade also hit the group hard, as investors probably no longer wanted to take risks across the entire market.

In my previous bullish FSK article, I highlighted the stock’s relative outperformance and undervaluation versus its peers, so I was confident that it should provide solid valuation support amid heightened competition in the BDC market.

In FS KKR’s second-quarter results release last week, concerns were raised about intensified competitive risks for FSK due to tighter spreads.There are fears that more capital Chasing less valuable opportunitieswhich raises concerns about the return of capital to potentially riskier portfolio companies. Macroeconomic headwinds have also increased as the market offers the possibility of Interest rate cut by 50 basis points at the Fed’s FOMC meeting in September.

The BDC showed a significant improvement in its non-accruals performance. Accordingly, FS KKR was able to significantly reduce its non-accruals, from 4.2% previously to 1.8% (based on fair value). On a cost basis, they fell from 6.5% previously to 4.3%. Management signaled the success of its restructuring efforts, particularly at Global Jet Capital. In particular, as a result of the restructuring, “$309.4 million in costs and $256.6 million in fair value” of the investment were taken out of non-accrual status.

FS KKR has also “achieved significant portfolio rotation out of cyclical industries” to further mitigate its portfolio risk profile. The BDC highlighted that more than $3 billion in “legacy investments” have been reallocated to “more defensive industries such as software and services, medical equipment and services, and commercial and professional services.” However, there is still a significant “12% risk in legacy investments” that the BDC must manage.

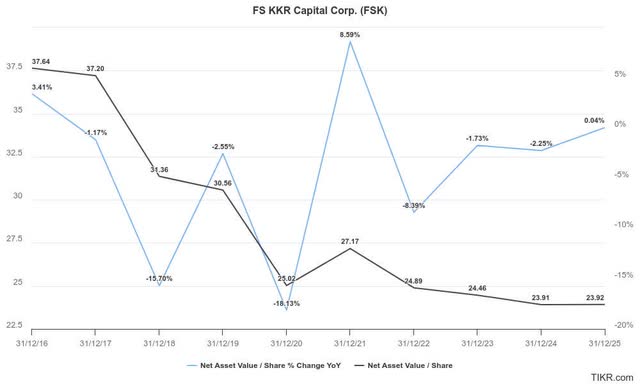

FSK estimates (TIKR)

I applaud management’s ability to manage the risks associated with non-accrual. However, the sequential decline in net asset value per share from $24.32 to $23.95 in the second quarter demonstrates the difficulty of maintaining investor confidence. In addition, Wall Street’s revised estimates suggest a further decline in fiscal 2024 as the company may continue to face near-term challenges in increasing portfolio value.

Nonetheless, Wall Street has upgraded its estimates of FSK, underscoring increased confidence in execution. Given the increasing macroeconomic headwinds, I expect execution risks in the BDC industry have also increased. Furthermore, if spreads continue to tighten without a corresponding decline in short-term funding costs, this could impact the company’s ability to deliver sustainable earnings growth.

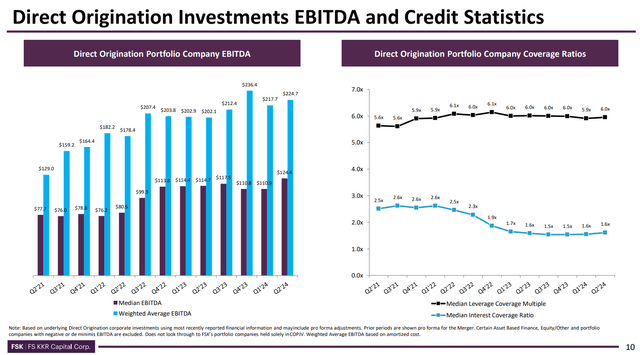

EBITDA and credit statistics for direct investments (FS KKR filings)

In addition, the market may further reduce its expectations for FSK and its BDC peers to reflect uncertain portfolio valuation assessments. Therefore, it is reassuring to know that EBITDA metrics and credit statistics for the FSK originations have remained relatively strong. This should give investors more confidence that the BDC is not aggressively seeking yield at the expense of portfolio quality. In addition, the exit from the legacy portfolio should also help strengthen the resilience of the FSK portfolio in the face of potentially stronger macroeconomic headwinds.

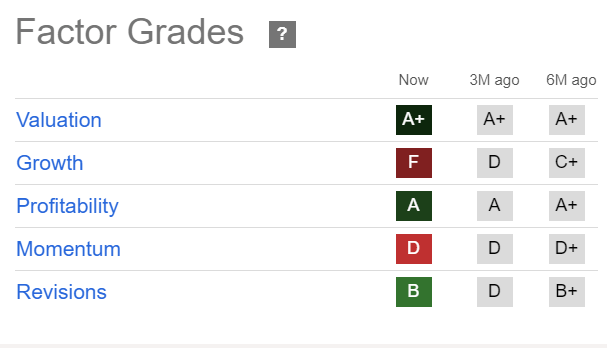

FSK Quant grades (Search Alpha)

FSK is still attractively valued at A+. In addition, Wall Street’s optimism about improved execution is reflected in the B rating on earnings revisions.

Therefore, I expect the market will likely monitor the trade-off between the expected decline in portfolio NAV for fiscal 2024 and its cheap valuation. The company will need to navigate a potentially less hawkish Fed starting in September 2024. As a result, FSK’s discount to its NAV per share will likely persist in the near term unless the BDC can demonstrate a more sustained improvement in its underlying portfolio performance.

In other words, I expect FSK to remain significantly undervalued in the near term, providing compelling investors with the opportunity to invest more heavily.

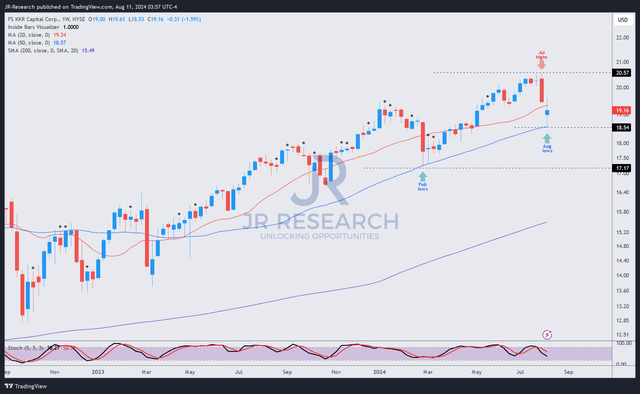

FSK price chart (weekly, medium-term, dividend adjusted) (TradingView)

FSK’s share price performance suggests that buying sentiment for the stock has remained incredibly robust. Over the past year, the stock has also taken advantage of price declines, underpinning investor confidence.

However, caution remains warranted as the Fed may adopt a more dovish monetary policy from September onwards. Execution risks to NAV growth are expected to remain even if pressure on funding costs for FSK’s portfolio companies should ease.

In addition, FSK is cheap and supported by a relatively attractive dividend yield of nearly 14%. Unless we enter a crippling period of a hard landing, I do not expect the market to devalue FSK significantly. Therefore, I remain constructive on the stock’s buy setups on dips and follow its upside bias.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not to rely on the information provided as financial advice. Consider this article as a supplement to your required research. Please always think independently. Note that the review is not intended to determine a specific entry/exit at the time of writing unless otherwise stated.

I want to hear from you

Do you have constructive comments to improve our thesis? Have you spotted a critical gap in our view? Have you seen something important that we missed? Do you agree or disagree? Post a comment below with the goal of helping everyone in the community learn better!

:max_bytes(150000):strip_icc():focal(748x222:750x224)/rebecca-cheptegei-budapest-082623-4820-edca1d5e0b2a4ae99b1f2f85a770dbbc.jpg "Olympic marathon runner Rebecca Cheptegei dies after petrol attack")