The Spanish corporate tax system has undergone significant changes over the decades, adapting to the changing economic landscape and the country’s evolving role within the European Union. Historically, Spain’s evolution from a closed economy under dictatorship to a liberalized market economy in the European context has required numerous reforms to its tax system. After Spain joined the European Economic Community in 1986, efforts began to adapt the corporate tax system to European standards, resulting in a series of reforms aimed at modernization and harmonization with international practices.

The evolution of the Spanish corporate tax system can be divided into different phases. Initially, the focus was on reducing high nominal tax rates and broadening the tax base to create a more efficient tax structure. Reforms in the early 1990s simplified the tax rate structure and reduced top tax rates to encourage investment and competitiveness. In the subsequent period, efforts were made to combat tax evasion and avoidance, culminating in a more robust and transparent corporate tax system (Oats and Tuck, 2019; Dey, 2020) (Figure 1).

Source: Authors’ analysis based on statistics from the Spanish tax authority.

The 2008 financial crisis triggered another wave of tax reforms designed both to raise revenues and promote economic recovery. Measures included adjustments to tax rates, the introduction of new deductions and incentives to promote growth and employment. In the period that followed, Spain faced the challenge of reconciling fiscal consolidation with the need to maintain an attractive environment for business and investment.

The current structure of the Spanish corporate tax system is a result of these continuous reforms. Following the latest updates, the standard corporate tax rate is at a competitive level compared to the EU average in order to attract foreign direct investment and encourage domestic economic activity. The tax system includes a range of deductions and credits, with a particular emphasis on innovation, research and development, and environmental sustainability.

Spain has also taken measures to align itself with the OECD-initiated project to combat base erosion and profit shifting (BEPS), including transfer pricing rules, controlled foreign company (CFC) regulations and restrictions on the deductibility of financial expenses.

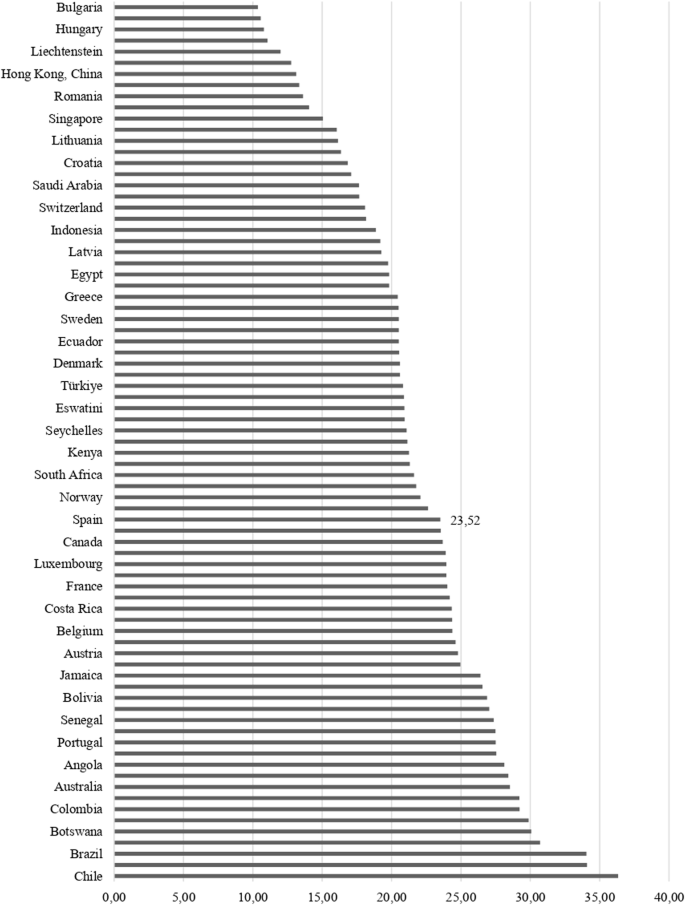

Figure 2 shows the average corporate tax rates in OECD countries and provides a comparative perspective that illustrates Spain’s position compared to other countries. This comparison highlights the need for Spain to remain competitive while ensuring sufficient revenues to support public services and economic development.

Source: The author relied on OECD statistics.

It is important to clarify the scope of the corporate tax base in the case of Spain, focusing in particular on the revenues generated from this tax. Corporate tax covers all companies that are legally obliged to declare their income in Spain in accordance with this provision. This tax base covers a wide range of corporate structures from different sectors, including limited liability companies, public limited companies and other legal entities that must participate in the tax system. Corporate tax revenues are significant because they capture the tax contributions of these companies and reflect their economic activities within the country’s borders.

The impact of this tax is profound as it directly influences the financial strategies of these companies. The data collected, which form the backbone of our analysis, therefore represents a comprehensive overview of the economic performance and fiscal contributions of the corporate sector in Spain. By analyzing this data, we aim to uncover patterns and impacts of corporate tax rate adjustments on total revenues and provide insights into the effectiveness and results of tax policies.

In summary, corporate tax revenue data from Spain, which include all legally required reporters, are a central element of our research. They allow a detailed examination of how corporate tax policies affect economic behaviour and revenue developments, thus providing valuable insights for economic analysts, policy makers and the wider financial community.

The historical evolution of the Spanish corporate tax system shows a consistent effort to balance revenue generation and economic competitiveness. These reforms have significant implications for current and future tax policy. Understanding these trends is crucial to identify areas where further adjustments may be needed to improve the efficiency and responsiveness of the system. The analysis of average corporate tax rates in OECD countries provides a comparative perspective and highlights Spain’s position compared to other countries. This comparison highlights the need for Spain to remain competitive while generating sufficient revenues to support public services and economic development.