stock?")

Are robust financials the reason behind the recent rise in Chenming Electronic Tech. Corp. (TWSE:3013) stock?

Chenming Electronic Tech (TWSE:3013) stock is up a remarkable 41% over the past three months. Given that the market rewards strong financials over the long term, we wonder if that is the case in this case. Specifically, we decided to examine Chenming Electronic Tech’s return on equity in this article.

Return on equity or ROE is an important factor for a shareholder to consider as it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio that measures the return on the capital provided by the company’s shareholders.

Check out our latest analysis for Chenming Electronic Tech

How do you calculate return on equity?

Return on equity can be calculated using the following formula:

Return on equity = Net profit (from continuing operations) ÷ Equity

Based on the above formula, the ROE for Chenming Electronic Tech is:

11% = NT$421 million ÷ NT$3.8 billion (based on the last twelve months ending June 2024).

The “return” refers to the profits of a company in the last year. You can imagine it like this: for every NT$ of shareholder capital, the company made NT$0.11 in profit.

Why is return on equity (ROE) important for earnings growth?

So far, we’ve learned that return on equity (ROE) measures how efficiently a company generates its profits. Depending on how much of those profits the company reinvests or “retains” and how effectively it does so, we can then assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the return on equity and earnings retention, the higher a company’s growth rate will be compared to companies that don’t necessarily have those characteristics.

Chenming Electronic Tech’s profit growth and return on equity of 11%

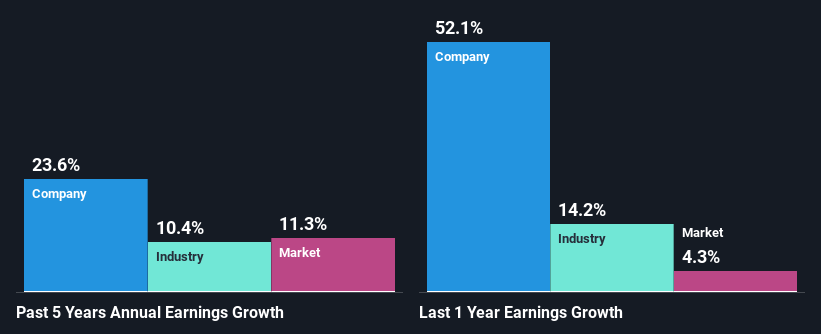

First of all, Chenming Electronic Tech appears to have a respectable return on equity. Even compared to the industry average of 12%, the company’s return on equity looks pretty decent. This probably explains, among other things, Chenming Electronic Tech’s significant net income growth of 24% over the past five years. We believe there could also be other aspects that are positively influencing the company’s earnings growth. For example, the company has a low payout ratio or is managed efficiently.

Next, when comparing with the industry’s net income growth, we found that Chenming Electronic Tech’s growth is quite high compared to the average industry growth of 10% over the same period, which is encouraging.

The basis for valuing a company depends largely on its earnings growth. The investor should try to determine if the expected earnings growth or decline, whichever may be the case, is built into the price. This will help them determine if the future of the stock looks promising or bleak. If you’re wondering about Chenming Electronic Tech’s valuation, check out this gauge of its price-to-earnings ratio compared to the industry.

Does Chenming Electronic Tech use its retained earnings effectively?

Chenming Electronic Tech’s three-year median payout ratio is rather low at 25%, which means that a high percentage (75%) of earnings is retained. So it seems like management is heavily reinvesting earnings to grow the business, which is reflected in the earnings growth number.

In addition, Chenming Electronic Tech has paid dividends over a period of six years, which means that the company is very serious about profit sharing with its shareholders.

Diploma

Overall, we think that Chenming Electronic Tech’s performance has been quite good. In particular, we like that the company reinvests a large portion of its profits at a high rate of return. This has naturally led to significant earnings growth for the company. However, when looking at the current analyst estimates, we found that the company’s earnings are expected to gain momentum. Are these analyst expectations based on broader expectations for the industry or on the company’s fundamentals? Click here to go to our analyst forecasts page for the company.

New: AI Stock Screeners and Alerts

Our new AI Stock Screener scans the market daily to uncover opportunities.

• Dividend powerhouses (3%+ yield)

• Undervalued small caps with insider purchases

• Fast-growing technology and AI companies

Or create your own from over 50 metrics.

Try it now for free

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.