")

Apple shares: Continue to lose market share in the smartphone sector (NASDAQ:AAPL)

Subscribe

Investment thesis

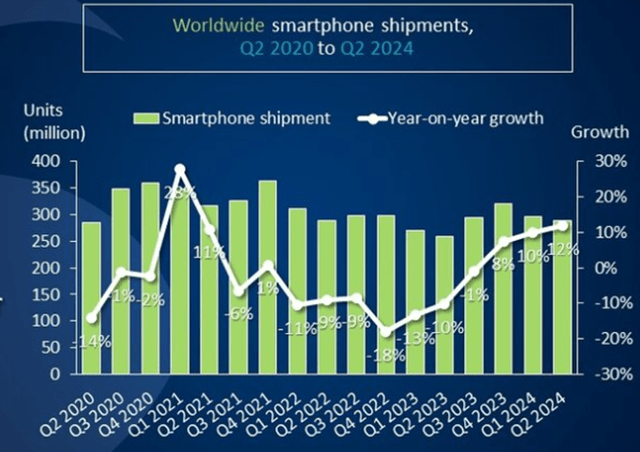

Demand in the global device market continued to recover. Apple (NASDAQ:AAPL) (AAPL:CA) sold 45.6 million smartphones in Q3 2024 (+6% YoY), while the overall smartphone market grew 12% YoY to 288.9 million units. Apple’s share of The smartphone market shrank by 16%, one percentage point less than the previous year. Falling sales in China were offset by rising sales in India. However, the iPhone is considered an expensive brand in the Indian market, so the compensation reduced average sales per customer to around USD 860 (-7% year-on-year).

In the last quarter, as we wrote in our previous article, Apple also lost market share in the smartphone market: In Q2 2024, Apple Inc. sold 48.7 million smartphones (-16% YoY), while the total smartphone market grew by 10% YoY to 296 million units. The rating is HOLD.

Smartphone market

Total smartphone shipments increased 12% year-over-year to 288.9 million units in Q2 2024 (Q3 2024 for Apple).

Canalys

Apple’s revenue was 45.6 million smartphones (+6% year-on-year), and Apple’s smartphone market share fell from 17% in Q2 2023 to 16% (Q3 2023 for Apple).

Developing countries in Asia, Latin America, Africa and the Middle East continue to be the main growth driver for the smartphone market, with physical sales there increasing by 10-20% year-on-year in Q2 2024. In monetary terms, however, Apple’s most important markets are the US, China and Europe. Total smartphone sales increased 5% year-on-year in the US, 14% in Europe and 6% in China. Despite this, Apple continued to lose market share in China, leaving it to local manufacturers. Apple’s market share in China fell to 15.5% from 17.4% last year, while physical sales fell 6%.

Luxury smartphone brands – Apple and Samsung – are benefiting from the market recovery in the US and Europe as old stocks are sold out and stores have started to restock them vigorously ahead of the new holiday season. In the second half of 2024, major brands will try to increase shipments of smartphones with GenAI on board. In the near future, this will be the main factor affecting the sales of a particular brand.

At a developer conference, Apple unveiled its own Apple Intelligence, which it plans to embed in smartphones and Siri to improve natural language understanding. In addition, Apple has partnered with OpenAI and will embed ChatGPT in its devices. According to insiders, the partnership with OpenAI is not for profit, meaning Apple will not pay OpenAI to use ChatGPT. Instead, OpenAI will gain access to Apple’s large customer base and will likely sell them mini-apps embedded in ChatGPT – transactions for which Apple will receive a 30% commission.

We expect that Apple’s integration with OpenAI will help it regain market share faster, especially in the US and EU. In developed markets, Apple competes primarily with Samsung, whose AI is weaker than ChatGPT. Apple will not have this advantage in the Chinese market, as the US tech giant will use Baidu’s AI there, which will provide a level playing field for local vendors.

In addition, we find that consumer spending in the US and Europe is actually exceeding disposable income, which is gradually eroding accumulated savings and depressing demand for durable goods.

Therefore, despite the rapid market recovery in the first half of the year, we maintain our forecast for smartphone shipments for the full year 2024 of 1.2 billion units (+5% year-on-year) and for 2025 of 1.26 billion units (+5% year-on-year).

Taking into account the integration between Apple and OpenAI, we increase the iPhone market share forecast from 19% (-0.9 percentage points) to 19.6% (-0.3 percentage points) for 2024 and from 19.3% (+0.3 percentage points) to 21.1% (+1.5 percentage points) for 2025.

The declining sales in China were offset by increasing sales in India. However, the iPhone is considered an expensive brand in the Indian market, so the compensation reduced the average revenue per customer to approximately USD 860 (-7% year-on-year).

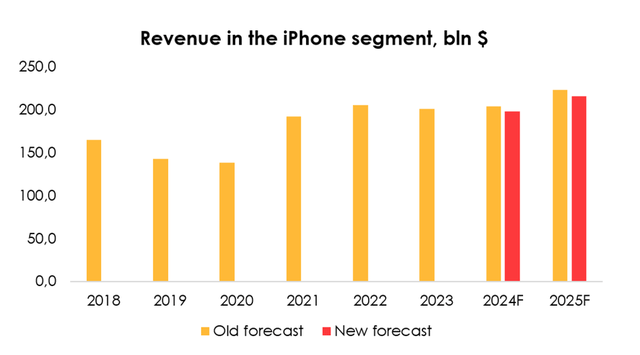

For this reason, we are lowering the forecast average revenue per iPhone from $935 (+3% YoY) to $886 (-2% YoY) for 2024 and from $982 (+5% YoY) to $884 (-0.2% YoY) for 2025.

Given all the changes, we are lowering Apple’s revenue forecast for 2024 from $203.6 billion (+1% yoy) to $198 billion (-1% yoy) and for 2025 from $223 billion (+10% yoy) to $215.6 billion (+9% yoy).

Heroes invest

Apple’s other segments

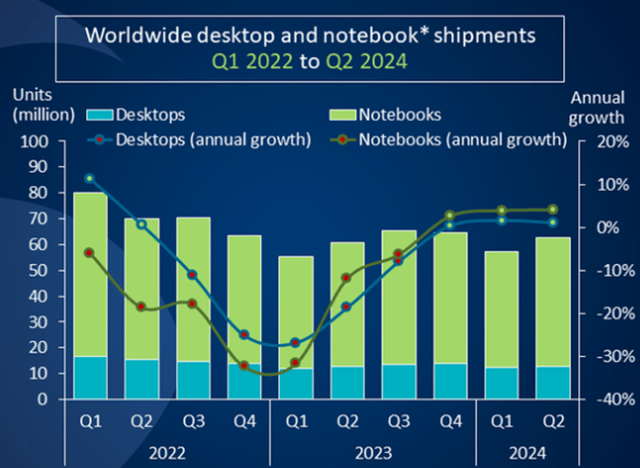

The Mac segment delivered stable financial results. Revenue in this segment totaled $7 billion (+2% year-on-year). The company sold 5.5 million Macs, up 6% year-on-year. Average revenue per unit decreased 2% year-on-year. Apple’s market share in the PC segment increased slightly to 8.8% (+0.2 percentage points year-on-year). The global PC market continued to recover at a moderate pace. Total PC shipments increased 3.4% year-on-year to 62.8 million units.

Canalys

The iPad segment began to recover rapidly, with revenue in this segment totaling $7.2 billion (+24% YoY). We attribute this to the release of the new iPad 2024 in May 2024. The new version of the iPad is far superior to previous versions and is powered by the revolutionary M4 chip. The tablet also includes an NPU Neural Engine, making it suitable for widespread use of AI apps.

Sales of wearable devices, which include the Apple Vision Pro, totaled $8.1 billion, down 2 percent from a year ago. Apple faces rapidly increasing competition in the smartwatch and wireless earphone market from Chinese rivals and the Nothing brand, which have made great strides in technology and design over the past year.

The company plans to sell Vision Pro in 8 more countries, including China and Japan. A new operating system has been announced for Vision Pro – VisionOS2. It will use machine learning to create spatial photos and offer new hand gestures. For now, Apple Vision Pro can be called an experimental model, which will be in demand primarily by companies that are trying to test it and adapt it to their own needs.

The company’s services revenue was $24.2 billion, an increase of 14 percent over the previous year.

Apple’s financial results

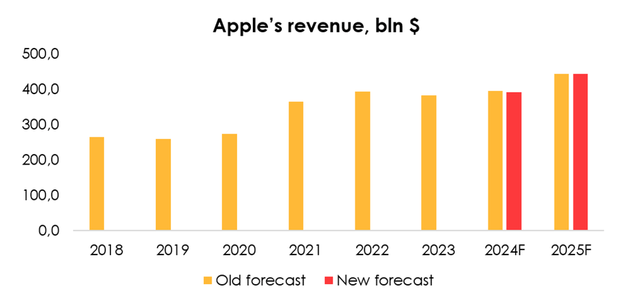

We are lowering our revenue forecast for Apple for 2024 to $391.3 billion (+2% year-on-year) from $395.6 billion (+3% year-on-year) and for 2025 to $443.8 billion (+13% year-on-year) from $444.7 billion (+12% year-on-year) due to expectations of weaker smartphone sales, although partially mitigated by higher forecasts for revenue in the iPad and Services segments.

Heroes invest

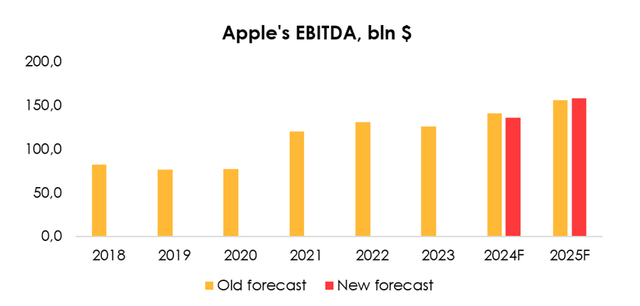

Due to the reduced revenue forecast and higher parts costs for the company’s devices, we are lowering EBITDA guidance for 2024 from $140.7 billion (+12% YoY) to $135.5 billion (+8% YoY) and increasing it slightly for 2025 from $155.8 billion (+15% YoY) to $157.7 billion (+16% YoY) due to the rapid growth of Apple’s peripheral services segment, which will offset the reduction in the company’s device revenue forecast.

Heroes invest

Evaluation

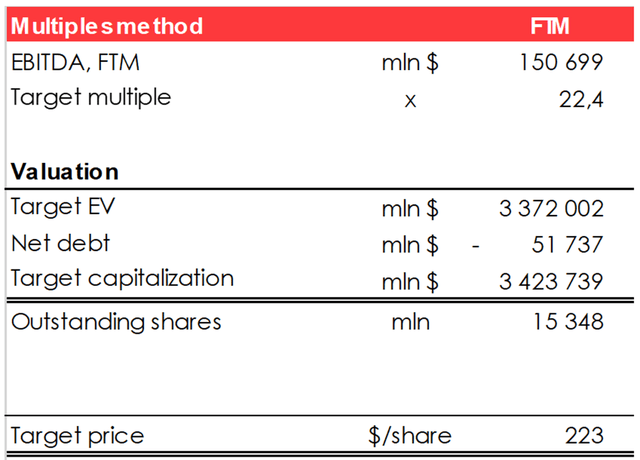

We are increasing the stock’s price target from $171 to $223 due to:

- increasing the target multiple for Apple from 17.5x to 22.4x;

- the reduced EBITDA forecast for 2024 and 2025;

- the increase in net debt from (58) to (52) billion US dollars;

- the reduction in the number of diluted shares outstanding from 15.5 billion to 15.4 billion;

- the postponement of the FTM assessment period.

We give the stock a “HOLD” rating.

Heroes invest

Diploma

Apple is a high-tech company that is building its own ecosystem. However, recent trends in the smartphone market are significantly limiting its growth potential. We expect the company to trade close to fair value and the rating is HOLD.

To manage your positions, we recommend that you follow Apple’s earnings releases and market updates.