")

Robert Way

Michael Burry, the investor known for his large short sales during the subprime mortgage bubble in 2007, has increased his stake in Alibaba (NYSE: BABA), according to the latest 13F filings of his company Scion Asset Management. He increased the The number of BABA shares he holds increased by 24%, while he reduced many other positions. BABA now takes up 21% of the portfolio and is Burry’s largest holding. Along with three other large Chinese stocks, Baidu (BIDU) and JD.com (JD) Chinese stocks account for about 45% of Burry’s holdings.

This seems bullish for Chinese large-cap stocks and Alibaba in particular. The dichotomy of investment opinion on Chinese stocks is quite interesting. Some simply consider China to be absolutely uninvestable, primarily because of the Chinese Communist Party and its firm control over all aspects of the country. It certainly doesn’t help that the world is going through deglobalization, the perception of US leadership is declining, China is trying to assert its dominance over Taiwan, and Xi Jinping is seemingly a stronger strongman and demagogue than anyone we have seen since Mao Zedong. Others believe this risk is greatly exaggerated and has driven Chinese stock multiples to lows that make it a highly valued security. For BABA, one can argue that the buybacks and ample cash position alone make the growth story very likely to play out. The rock-bottom valuations are just an additional margin of safety.

While I tend to lean toward the former, I believe there are times when sentiment makes it sensible to take speculative positions. I think this could be one of those times. Both BABA stock and China’s large-cap index FXI have been punished by the market in recent years.

BABA and FXI (Search Alpha)

BABA trades at very attractive valuations despite its high profitability. In fact, BABA has an overall profitability grade of A+ on Seeking Alpha and performs quite well on most common valuation metrics such as PEG, PE, EV/EBITDA and PB ratios.

Buybacks and dividends

The most optimistic fundamental development is probably buybacks. BABA is increasing buybacks and has retired 5% of its shares in fiscal 2024. Buybacks are the perfect way to return cash to shareholders as they are not taxed until the shares are sold at a profit. BABA also started paying a dividend in early 2024 and has a payout ratio of just 11.7%, making this cash flow very safe.

BABA has a very strong cash position. Its most recent balance sheet shows $12.68 cash per share. It also shows free cash flow per share of $7 and earnings per share of $3.86. I think the buybacks and dividends are pretty safe based on that alone. The dividend rate is only $2 per share. If just half of the remaining $5 of the $7 free cash flow goes to buybacks, the cash per share will increase dramatically.

Currently, BABA has only spent $5.8 billion on buybacks from last quarter. This reduced the share count by 2.3%. $5.8 billion is less than a third of the TTM free cash flow of $19.4 billion. With a significant cash balance and a fantastic cash flow situation, this current pace of buybacks could probably be maintained for a while. It’s hard to see how the price can continue to stay low with all this buying pressure driving it higher.

Chinese extreme risk

Of course, the CCP is the big problem here. If China occupies Taiwan, we can expect Chinese stocks to be taken off Western markets, which is exactly what happened with Russian stocks in 2022. In this case, BABA shareholders (as owners of the ADR) will be completely wiped out, although the real Alibaba shares could still be traded in Hong Kong.

This extreme risk is important to consider. China has been conducting provocative military exercises around Taiwan. The frequency of such exercises appears to have increased over time. Xi Jinping has only recently declared that the two countries are destined for reunification. Given that Xi is already 71 years old and may want to be the leader who carries out this “destiny”, I think we need to be very cautious about this particular risk.

Another tail risk is that the Chinese economy is probably not doing so well. The CCP is not all that transparent about the way it reports numbers, and many of its planned economy policies have started to backfire spectacularly. Evergrande, for example, is a relatively recent example of immense value destruction that was ultimately caused by the CCP’s intention to artificially inflate GDP numbers. We can hardly know what kind of contagion might be lurking beneath the surface. What we do know is that average Chinese are starting to buy physical gold as a safe haven. This is definitely a sign of widespread bad sentiment, and often this can be a self-fulfilling prophecy.

The smaller risk is that weakness in Chinese consumers will hurt Alibaba’s sales. As a consumer goods company, BABA does not benefit from low demand elasticity. A weaker Chinese economy would affect much of BABA’s cash flows. Sentiment would deteriorate and buybacks would have to slow down, negating the core thesis of cash flow-induced buying pressure on the stock.

The much bigger risk is that the CCP’s best move to distract the population from a declining economy might be to attack Taiwan. This would be an extremely sensible political move. Any economic misery caused by the deteriorating Chinese economy could be blamed on the rest of the world imposing sanctions on China. Plus, Xi would finally have a chance to force reunification.

The trade

I think OTM call options might be the most appropriate trade here. You can limit your downside risk to the premium of the option. This would be insurance in case the tail risks materialize. Sentiment is pretty bad right now, so it might pay to be a contrarian, and the lower upfront cost of buying a call is perfect for a highly asymmetric bet.

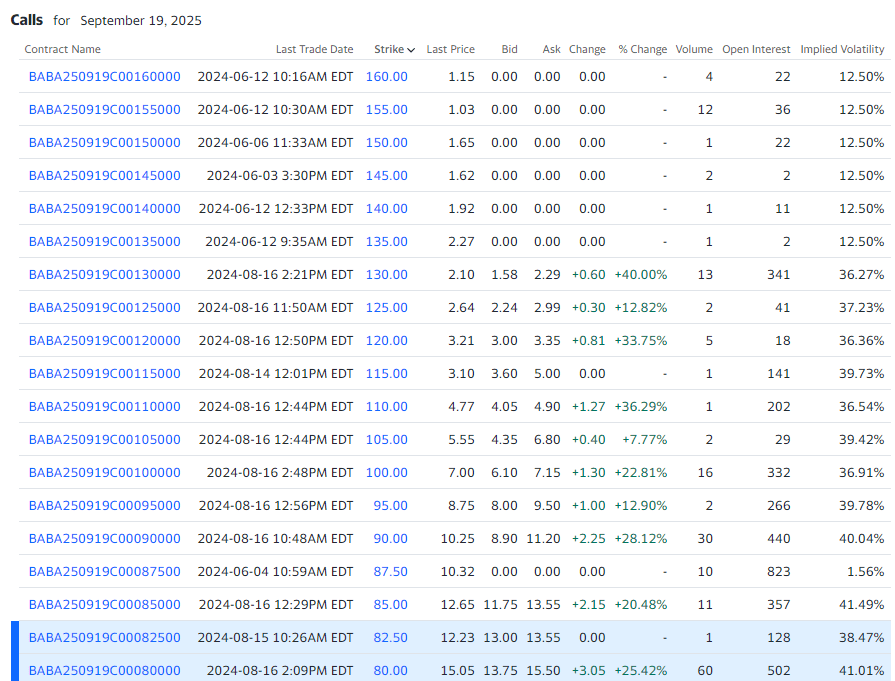

BABA OTM calls (Yippee!)

I think BABA acted pretty reflexively. Already in 2021, the sentiment around all Chinese stocks started to deteriorate, and over the past three years, this has continued to accumulate. If the buybacks continue to push the price higher and thereby change the sentiment, we could probably see a rise to $120 per share, which is about 50% above where we are now. Therefore, buying the BABA 120 call expiring September 2025 for $320 would be a good deal.

The nice thing is that BABA’s calls are priced at lower implied volatilities as strikes move higher. This could be a sign of quite depressed sentiment. Any sort of upward appreciation could drive up the value of OTM calls by reassigning them with a higher IV.

The current ATM call expiring in 4 months is around $800, so if BABA is at 120 within 6 months, this contract could more than double. The weakness is that time decay is very real in OTM options. Every day that BABA stays at current levels will eat away at the main investment. So this is a high risk, high reward trade where one intentionally limits one’s losses because one is aware of the current tail risks.