Flight Centre Travel Group (ASX:FLT) has had a rough month, with its share price falling 8.2%. But if you look closely, you’ll see that its key financial indicators are looking quite good, which could mean the stock could potentially rise in the long term, as markets typically reward steadier long-term fundamentals. In particular, we’ll be paying attention to Flight Centre Travel Group’s return on equity today.

ROE, or return on equity, is a useful tool to assess how effectively a company can generate returns on the investments it receives from its shareholders. In short, ROE shows the profit each dollar generates in relation to its shareholder investments.

Check out our latest analysis for Flight Centre Travel Group

How do you calculate return on equity?

Return on equity can be calculated using the following formula:

Return on equity = Net profit (from continuing operations) ÷ Equity

Based on the above formula, the ROE for Flight Centre Travel Group is:

13% = AU$154 million ÷ AU$1.2 billion (based on the trailing twelve months to December 2023).

The “return” is the annual profit. You can imagine it like this: for every Australian dollar of shareholder capital, the company generates 0.13 Australian dollars in profit.

What does return on equity (ROE) have to do with earnings growth?

We have already established that return on equity (ROE) serves as an efficient measure of a company’s future earnings. Now we need to evaluate how much profit the company reinvests or “retains” for future growth, which then gives us an idea of the company’s growth potential. Assuming everything else remains unchanged, the higher the return on equity and retained earnings, the higher the growth rate of a company will be compared to companies that do not necessarily have these characteristics.

Flight Centre Travel Group earnings growth and return on equity (ROE)

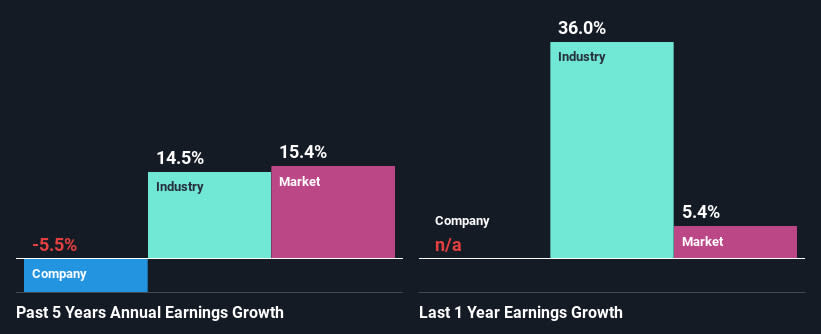

At first glance, Flight Centre Travel Group appears to have a decent return on equity. Moreover, the company’s return on equity is in line with the industry average of 12%. Although Flight Centre Travel Group has a fairly respectable return on equity, its net income decline rate over five years was 5.5%. So there could be other aspects that could explain this. For example, it could be that the company has a high payout ratio or the company has allocated its capital poorly.

We then compared Flight Centre Travel Group’s performance with the industry and were disappointed to see that while the company has suffered a decline in profits, the industry has seen gains of 15% over the past few years.

The basis for valuing a company depends largely on its earnings growth. It is important for an investor to know whether the market has priced in the company’s expected earnings growth (or earnings decline). This will help them determine whether the stock’s future looks promising or bleak. What is FLT worth today? The intrinsic value infographic in our free research report helps visualize whether FLT is currently mispriced by the market.

Does Flight Centre Travel Group use its retained earnings effectively?

Given the three-year median payout ratio of 48% (or a retention ratio of 52%), which is fairly normal, Flight Centre Travel Group’s declining earnings are quite puzzling, as one would expect significant growth when a company retains a good portion of its earnings. So there could be other factors at play that could potentially hinder growth. For example, the company has been battling some headwinds.

Furthermore, Flight Centre Travel Group has been paying dividends for at least ten years, suggesting that maintaining dividend payments is far more important to management, even if it comes at the expense of business growth. Based on the latest analyst estimates, we found that the company’s future payout ratio is expected to remain stable at 53% over the next three years. However, forecasts suggest that Flight Centre Travel Group’s future return on equity will increase to 22%, although the company’s payout ratio is not expected to increase significantly.

Diploma

Overall, we think that Flight Centre Travel Group does have some positive factors to consider. However, given its high return on equity and high profit retention, we would expect the company to deliver strong earnings growth, but that is not the case here. This suggests that there could be an external threat to the company that is hindering its growth. With that in mind, the latest industry analyst forecasts show that the analysts are expecting a huge improvement in the company’s earnings growth rate. You can find more information on the company’s future earnings growth forecasts here free Read the company’s analyst forecasts report to learn more.

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

:max_bytes(150000):strip_icc():focal(749x0:751x2)/Jean-Smart-2024-Emmys-091524-4a8a8bd254a64332a3b53b990abf7200.jpg "Jean Smart jokes she’ll win the 2024 Emmys, saying she “doesn’t get enough attention”")