")

Subscribe

The S&P 500 (SPY) continued its recovery rally to nearly the previous all-time high and then fell sharply on Thursday. A double top? The start of the next big slump?

These are probably the wrong questions when the context is bullish. The most useful question is surely: where can I buy the dip? As I will show later, the answer is often simple.

This week’s article will highlight key levels for the S&P 500 to hold on to during dips. It will also take a closer look at the current pattern and speculate on what might happen now that we are back near the all-time highs. A top-down process will apply various techniques to multiple time frames, while also considering key market drivers. The goal is to provide an actionable guide with directional bias, key levels and expectations for future price action.

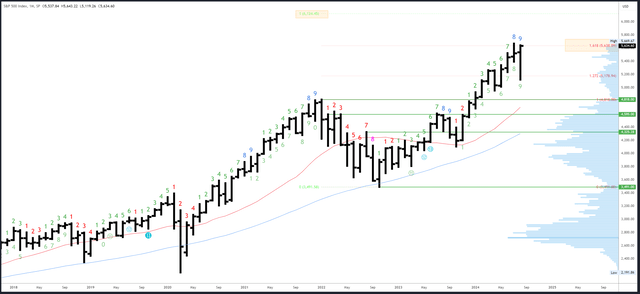

S&P 500 monthly

New August highs have been reached and with 1 week to go until the month close, a bullish bar looks very likely to form. Only a close below 5390 would shift the bias neutral/bearish.

It was interesting to see that the major Fibonacci extension of 5638 (mentioned in most articles since June) was still in effect as the S&P 500 made a sharp decline from 5643. I guess this won’t be the last time this area will be relevant.

SPX monthly (Tradingview)

5638 and the top of 5669 are potential resistance points. The next key target for new highs is the 6124 mark. This is a measured move that will see the 2022-2024 rally be as big as the 2020-2022 rally. It is unlikely to be reached before the election, but it is a possible target at some point in this bull market.

5390 and the August low of 5119 are initial supports.

The August bar will complete Denmark’s upside exhaustion. The nearly 10% correction may have already deepened, but its impact could linger and limit pre-election price rallies.

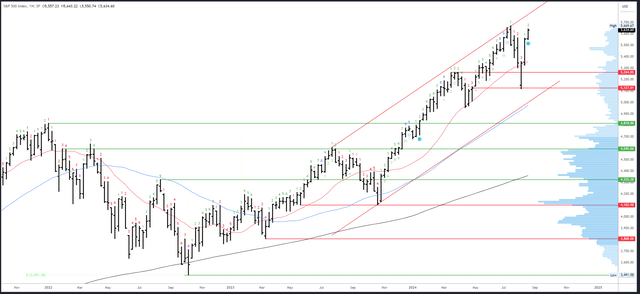

S&P 500 weekly

Friday’s rebound saved the weekly bar from a bearish/neutral shift (closing below the open of 5557). Another higher low, higher high and higher close were formed and we now have a clean 3-bar rally from the lows. Markets tend They move in sequences of 3 bars (at least on the weekly and daily timeframes) and often get stuck at bar 4. Chances are we’ll see an initial rally next week, but it will likely stall below the all-time high of 5669.

SPX weekly (Tradingview)

5669 is the only resistance. 6010 is the 161.8* Fibonacci extension of the July-August decline.

5550 is the initial support. Below that, there is no convincing weekly support until 5324-5358. The 20-week MA will rise to around 5380 next week.

Next week will mark bar 3 (out of a possible 9) in a new countdown of Denmark’s exhaustion.

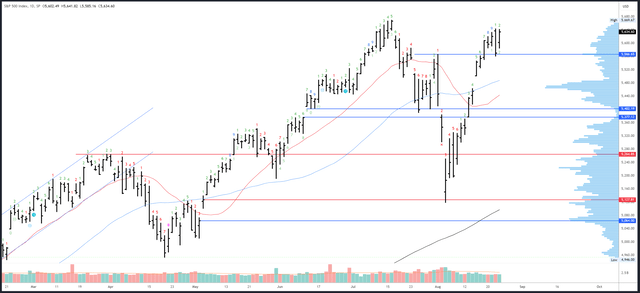

S&P 500 daily

The S&P 500 continues to break through potential resistance. Last week’s 5566 level offered no challenge at all on the way up and served as support on Thursday’s breakout to spite the bears. This was an easy level drawn at the high before the “crash.”

SPX daily (Tradingview)

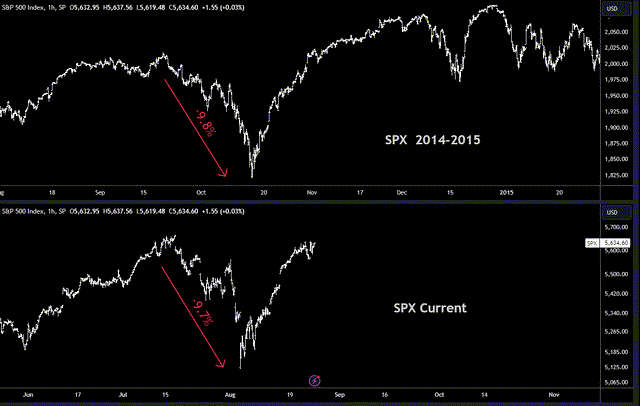

A clear “V” pattern has formed from the July/August decline and recovery. Historical charts show that the “V” pattern is common in the S&P 500, but the recovery usually does not reach the previous peak in such a short time. It was similar in November 2023, but the most compelling comparison of the same magnitude is from 2014, when there was a -9.8% decline that recovered in 3 weeks, just like now.

SPX vs 2014 (Tradingview)

If the comparison continues, the forecast price path ahead of the election seems logical. A breakout to new highs is likely, but momentum is likely to fade and gains are likely to be limited given stretched valuations and slowing growth. Volatility could well increase in late September and October, bringing several sharp declines (and rebounds).

Obviously, this is just speculation and is not essential for successful trades. We just need to know where the next drop is expected.

5550-5560 is the first support. The gap at 5500 is more important, with the 50-day moving average rising to 5492. The 5390-400 area is still relevant, but a return to this area would reflect a weak trend and challenge the expected breakout.

An upward exhaustion in Denmark was completed last Wednesday and contributed to Thursday’s decline. No new exhaustion signals can occur next week.

Drivers/Events

Fed Chairman Powell used his speech in Jackson Hole to confirm that a rate cut will happen in September. However, it is still unclear whether the cut will be 25 or 50 basis points, and markets are still assuming a 25 percent chance of a 50 basis point cut. Everything depends on the upcoming data, especially the next employment report, which is expected on September 6.

While equity markets are expected to favor a 50 basis point cut, this is not necessarily the case if it is driven by a deterioration in the labor market. Equities would likely prefer a solid economy and a slower easing cycle.

Next week’s data will be quiet again. Preliminary GDP and unemployment figures will be released on Thursday, but will not affect the outcome of the September FOMC meeting. The PCE index will be released on Friday and is expected to show a modest reading of 0.2%, confirming that inflation is a receding problem.

Possible steps next week(s)

Overall, sentiment remains optimistic and a breakout to new all-time highs is expected in the coming weeks. Only a break below 5500 would endanger the uptrend, and even then 5390-5400 could be enough for a sideways consolidation.

After three strong weeks, some loss of momentum is to be expected and consolidation in the 5550-5669 range would be healthy. However, the strength of the recent relief rally is not commonplace and the “V” pattern can be compared to October 2014 when it continued to make new highs with very minor dips. The projected path from this comparison seems logical – an initial rise to new highs could slowly continue, but gains are likely to be capped at 5900-6000 and could fade again with a series of sharp declines just before the election.

In the short term, Friday’s measures forecast a continuation of the uptrend early next week. 5,669 is the obvious target and could lead to some slight volatility in what is likely to be a quiet period before the crucial employment report on September 6.