")

Lobro78

introduction

Three months ago I shared my “Strong Buy” recommendation for Apple (NASDAQ:AAPL). AAPL has gained about 18% since May, comfortably outperforming the S&P 500. Apple’s brand and pricing power are intact, and the company recently launched its groundbreaking iOS18 with AI features. Apple continues to bet heavily on innovation by investing billions in R&D, and investors are likely to see several promising new product releases soon. In addition, turning points in developed markets’ monetary policies are coming, so I believe iPhone sales growth will pick up again. Apple also continues to benefit from the strength of its ecosystem and intact brand power as service revenues continue to grow. I still believe AAPL is a “Strong Buy” and I’m adding more shares to my position as my valuation analysis suggests 30% upside potential.

Fundamental analysis

Apple is firm Innovation is the company’s goal. 8 billion dollars spent on research and development during the last reportable quarter. R&D investments are paying off as there have been several important software releases since I last wrote. The company introduced a new WWDC2024. The most important aspect is that the updated iOS will use generative AI features, which means that criticism of Apple’s presence in the AI revolution has not gone down well. At the same event, Apple also unveiled software updates for iPad, Mac, Watch and VisionPro.

Recent reports suggest that investors can expect the release of more new products soon. According to Seeking Alpha, the company is working on a redesigned Mac mini that will feature a powerful M4 chip. This chip in the design means that the updated product will utilize AI capabilities, which is in line with the evolving technological landscape. The company is also working on a tabletop robot, and this device could be launched as early as 2026. There is a lot of uncertainty here, but at the same time, the robot market could be a new strong growth opportunity. According to the same source, the company is also working on several other interesting products such as “augmented reality glasses; smart glasses similar to Meta’s (META) Ray-Ban glasses; a version of its popular AirPods headphones with cameras; and a foldable iPad.”

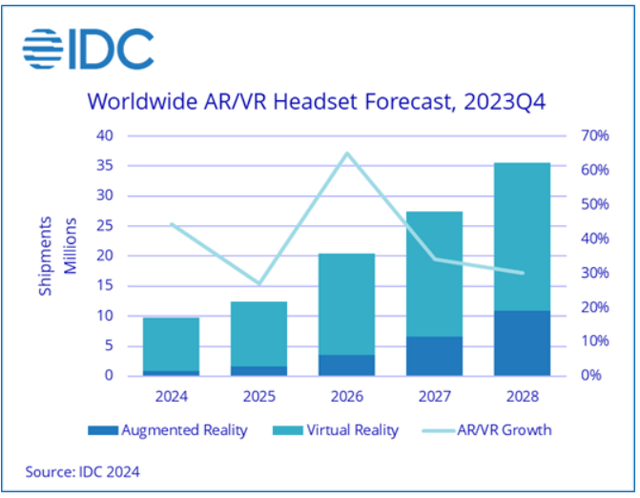

Management also shows its commitment to fully exploit the potential of the Vision Pro headset. The product is now officially available in countries with large economies such as China, Hong Kong, Japan and Singapore. Apple is also working on a lower-cost version of Vision Pro, which is expected to be unveiled in 2025. These developments are also positive, as IDC predicts strong growth in AR/VR headset shipments over the next five years.

IDC

Apple’s release of Q3 2024 results is another key development that supports my bullish stance. Revenue grew 4.87% year-over-year, while non-GAAP earnings per share increased from $1.26 to $1.40. The quarter was not flawless from a revenue perspective, with only Services and iPad seeing strong year-over-year growth. There was also modest year-over-year growth in Mac, but the contribution was insignificant in absolute terms.

Apple’s 10-Q report

AAPL bears will likely say that sales momentum is not so optimistic as iPhone and wearables sales continue to stagnate. However, I am confident that the headwinds for these categories are likely to be temporary due to the current unfavorable macro environment. While owning a smartphone is essential in the modern world, upgrading from the iPhone 14 to the iPhone 15 is a discretionary expenditure as such a purchase can be easily postponed without compromising quality of life. As households across the developed world continue to suffer from high interest rates, their discretionary spending is deteriorating.

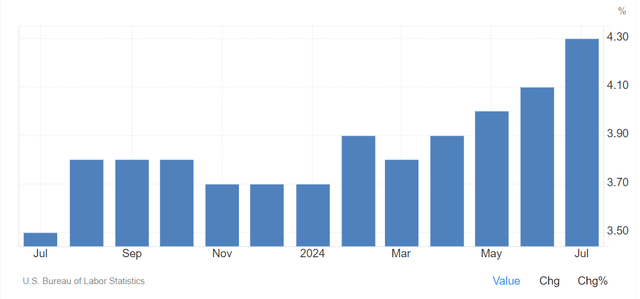

Inflation fell below the important psychological mark of 3% in July, which is quite a good development that probably comes close to positive changes in the monetary environment. The Fed has not started cutting rates yet, but the fact that inflation is now below 3% makes the start of rate cuts much closer anyway. The fact that the US unemployment rate rose from 4.1% in June to 4.3% in July is another valid reason for the Fed to start easing monetary policy due to its “dual mandate”. The US unemployment rate is clearly showing an upward trend, as shown below. Nevertheless, I expect demand for Apple products to pick up again as monetary policy in developed countries becomes less restrictive.

Trade economics

Overall, I see no reason to be less optimistic about AAPL. The iPhone sales headwinds are temporary and will most likely dissipate soon. The company is working on developing several promising products and I firmly believe that the WWDC2024 presentation was a game-changing event that changed the market’s perception of Apple’s ability to drive the AI revolution. The company’s ecosystem and brand loyalty are helping it grow earnings per share quickly despite some temporary revenue challenges, meaning the company’s moat is still intact.

Valuation analysis

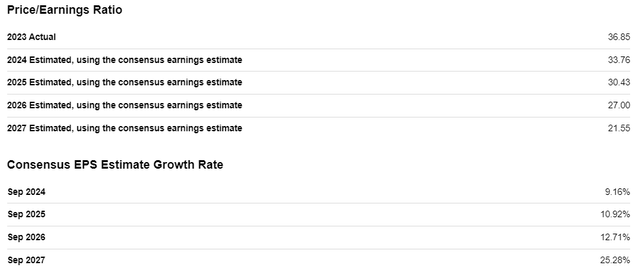

Apple is a unique company that has no competitors that have a comparable ecosystem of products and services. Therefore, it seems impossible for me to find a company whose valuation metrics I can compare to Apple’s. Therefore, looking at the company’s P/E ratio’s likely trajectory over the next few years will provide a better understanding of the company’s valuation. As shown in the screenshot below, the P/E ratio is expected to decline significantly over the next five years. This means that the current valuation is reasonable given the EPS growth potential.

S.A.

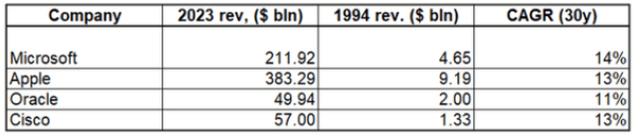

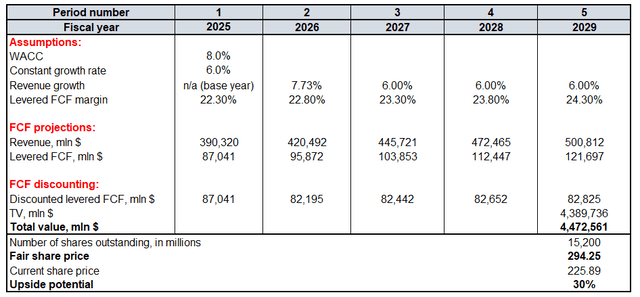

Discounted cash flow (“DCF”) analysis will help me determine AAPL’s fair stock price. Future cash flows are discounted using a WACC of 8.0%. Since my previous thesis has aged well, I confirm a 6% consistent growth rate for my DCF model. Bears will definitely question my 6% consistent growth rate in comments, but I insist that this value is conservative for an unprecedented ecosystem like Apple. My analysis suggests that Apple has achieved a revenue CAGR of over 10% over the past three decades. Furthermore, the compilation below shows that Apple has not been the only company to sustain a double-digit revenue CAGR over the past three decades. With all due respect to companies like Oracle (ORCL) and Cisco (CSCO), their business models do not leverage an ecosystem as vast as Apple’s. Still, AAPL’s revenue CAGR over the past three decades, coupled with the tremendous potential in AI following the release of iOS 18, makes me confident that a consistent 6% growth rate is solid.

Compiled by the author

When forecasting a constant growth rate, we should also keep in mind that companies have the ability to grow through acquisitions. Of course, if companies could only achieve organic growth, my forecast constant growth rate would have been in line with average GDP growth rates. For example, Apple acquired 32 AI startups in 2023. These acquisitions helped Apple integrate AI features into its iOS 18. In summary, I believe that the ability of companies to grow through mergers and acquisitions is a powerful catalyst that helps companies increase their revenue growth beyond GDP growth levels.

It makes sense to rely on the revenue consensus for fiscal year 2024-2025, as I believe the sample of around 40 Wall Street analysts is representative. For the years after 2025, I use the same 6% compound annual growth rate, which is the consistent growth rate. I use a TTM FCF margin of 22.3% for the base year and expect it to increase by 50 basis points annually. My confidence in Apple’s ability to improve its FCF margin is based on the company’s historically strong operating leverage.

Compiled by the author

My fair share price estimate is $294, which is 30% higher than the current share price. A 30% discount for a stock like Apple is a bargain in my opinion.

Mitigating factors

There is a risk that my fundamental analysis is missing something important, as Warren Buffett’s Berkshire Hathaway (BRK.B) has significantly reduced its stake in Apple according to recent reports. Warren Buffett is considered the greatest investor of all time and all his moves are most likely well-considered. The similarity between my opinion and that of Mr. Buffett could mean that I have overlooked some fundamental errors in my analysis. On the other hand, my bullish assessment of Apple has never disappointed me so far.

According to the company’s revenue breakdown below, China is the third-largest market for Apple. As we can see in the breakdown, the Chinese segment was the only one that saw a decline in revenue in Q3. This is due to geopolitical difficulties and increasing competition from Huawei in smartphones. Apple even lost its top-5 spot in China recently. On the other hand, Apple is not willing to continue losing market share in this important market and has huge resources to keep the fight going. Moreover, the expected release of the AI-powered iPhone 16 in September will likely help improve Apple’s competitive position against aggressive local players like Huawei.

Apple’s 10-Q report

Diploma

A stock like AAPL at a 30% discount is a no-brainer. I expect more promising new products and updates soon. Monetary easing in North America and the Eurozone will also likely help close the gap between the current share price and its fair value.