Global markets have proven resilient recently, with U.S. stocks recovering after a significant sell-off and growth stocks outperforming value stocks, driven by strong performance in the technology sector. Amid these market dynamics, insider ownership can be a valuable indicator of confidence in a company’s long-term prospects. In this context, identifying growth companies with high insider ownership and notable revenue growth can provide unique insights into potential investment opportunities.

Top 10 growth companies with high insider ownership

| name | Insider ownership | Profit growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| Seojin System Ltd (KOSDAQ:A178320) | 30.5% | 52.1% |

| Medley (TSE:4480) | 34% | 30.4% |

| KebNi (OM:KEBNI B) | 37.8% | 86.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.1% | 95% |

| Adocia (ENXTPA:ADOC) | 11.9% | 63% |

| Adveritas (ASX:AV1) | 21.1% | 144.2% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 100.3% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.5% |

Click here to see the full list of 1,504 stocks from our Fast-Growing Companies with High Insider Ownership screener.

Below we present some of our favorites from our exclusive screener.

Simply Wall St Growth Rating: ★★★★☆☆

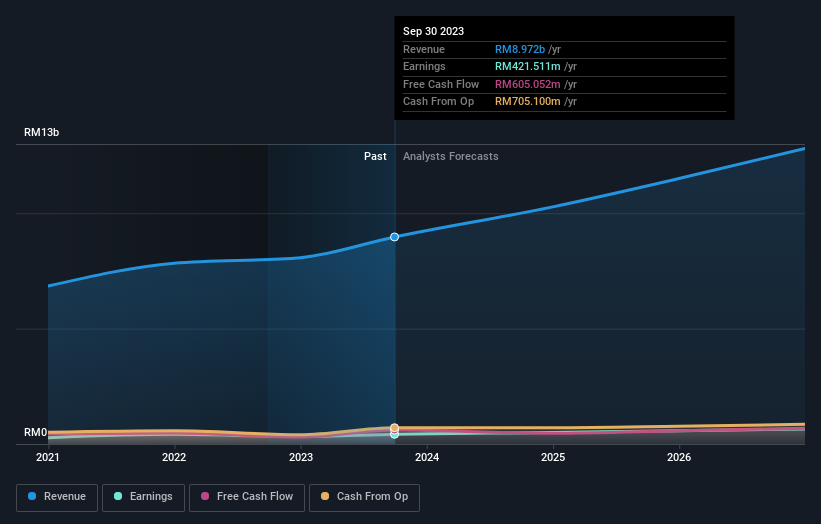

Overview: 99 Speed Mart Retail Holdings Berhad, an investment holding company with a market capitalization of MYR 15.96 billion, operates mini-supermarkets in Malaysia.

Operations: The turnover of the department stores is 8.97 billion MYR.

Insider ownership: 31.5%

Sales growth forecast: 10.8% per annum

99 Speed Mart Retail Holdings Berhad, a growth company with high insider ownership, has shown strong financial performance. Its revenue is expected to grow 10.8% annually, outperforming the Malaysian market at 6.2%. Earnings grew 20.4% last year and are expected to grow 13.29% annually, outperforming the market at 10.6%. Its recent IPO raised MYR2.36 billion, supporting further expansion. Trading at an attractive valuation below fair value increases the company’s attractiveness for investment.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Will Semiconductor Co., Ltd. is a semiconductor design company providing sensor, analog, touch screen and display solutions with a market capitalization of CNY 101.72 billion.

Operations: Revenue segments (in million CN¥): Sensor solutions: 5,600; Analog solutions: 3,200; Touch screen and display solutions: 2,400. Will Semiconductor generates revenue from sensor solutions (5.60 billion CN¥), analog solutions (3.20 billion CN¥) and touch screen and display solutions (2.40 billion CN¥).

Insider ownership: 30.7%

Sales growth forecast: 13.8% per annum

Will Semiconductor has shown significant growth. Revenue in the first half of 2024 was CNY 12.09 billion, up from CNY 8.86 billion last year, and net profit increased from CNY 153.12 million to CNY 1.37 billion. Earnings are expected to grow 38.7% annually over the next three years, outpacing the Chinese market’s growth rate of 23%. Despite lower future return on equity forecasts (17.3%), analysts expect the share price to rise by around 46.7%.

Simply Wall St Growth Rating: ★★★★☆☆

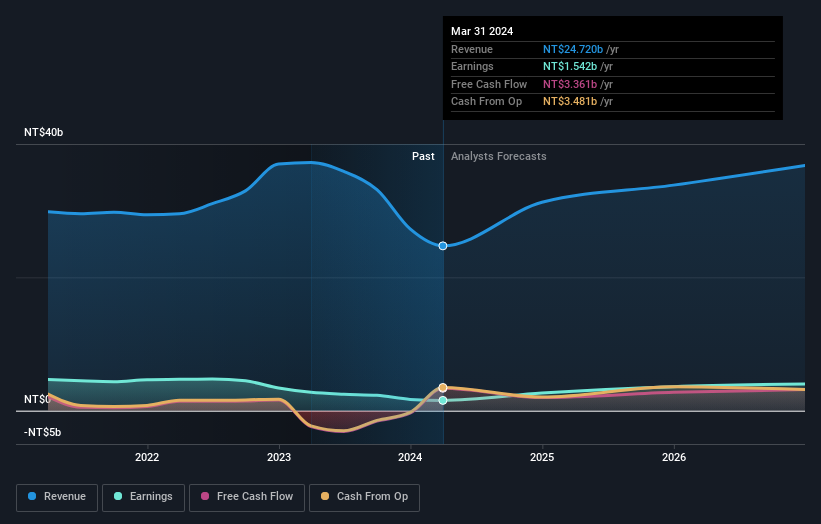

Overview: Merida Industry Co., Ltd. manufactures and sells bicycles and components in Taiwan, China, Hong Kong, Japan and Europe with a market capitalization of NT$66.08 billion.

Operations: Revenue from the manufacture and sale of bicycles and bicycle parts amounts to NT$26.58 billion.

Insider ownership: 26.8%

Sales growth forecast: 12.7% per annum

Merida Industry’s latest earnings report showed mixed results. Revenue in the second quarter of 2024 increased to TWD 9.32 billion from TWD 7.46 billion last year, but net profit declined slightly from TWD 671.77 million to TWD 655.55 million. Despite this, it is forecast to deliver significant earnings growth of 34.6% per year over the next three years, outpacing the Taiwan market’s growth rate of 18.4%. High insider ownership and significant expected earnings growth make the company an interesting prospect for investors looking for growth opportunities.

Take advantage

Looking for a new perspective?

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. This is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not own any shares in the stocks mentioned. The analysis only considers shares held directly by insiders. It does not include shares held indirectly through other vehicles such as corporations and/or trusts. All forecasted sales and earnings growth rates refer to annualized (per year) growth rates over 1-3 years.

Valuation is complex, but we are here to simplify it.

Find out if Will Semiconductor could be undervalued or overvalued with our detailed analysis, Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you interested in the content? Contact us directly. Alternatively, send an email to [email protected]